During the spring and summer months, bidding wars are rampant, there’s fierce competition, and a large pool of buyers are looking to move before the school year begins.

But in winter, especially in colder climates when everything is covered in snow, sellers and buyers alike can also take advantage of the season to score a good deal on real estate. Experts say that the idea that homes are very tough to sell or buy in the winter might be a myth. When temperatures drop, the market could be full of eager sellers and serious buyers who are both looking to score a cold, sweet deal.

Advantages for Sellers

You have less competition

Since there are fewer homes on the market, you have less competition from other sellers. The low inventory creates increased competition among buyers, which generally result in higher sale prices. This is why winter can also be an ideal time to sell your home.

You will show your home to a pool of serious buyers

When you put your home in the market during the winter months, there’s a greater chance you’ll attract a pool of real buyers looking to purchase and not those window shoppers who are just curious about the house. These serious buyers want to take advantage of the less competitive market and don’t want to wait until spring to get their hands on their ideal home.

You can highlight that your home is winter-ready

Aside from cozy fireplaces, hot tubs, and steaming mugs of hot chocolate with freshly baked cookies that await buyers when they tour your home, you can feature your house’s winter-readiness when you sell in the colder months. Show off the design and features that will make their life easier during winter, like an easy-to-shovel driveway, new roof and furnace, south-facing windows, and well-insulated pipes, among other things. These features, however simple, will show that your home can handle the harsh elements.

Many buyers are looking to relocate

People often look to relocate at the start of the year, especially those with new job opportunities, or young parents who want to start the new year somewhere in a more spacious family home. These buyers are serious about the sale and want to secure the property before Christmas or New Year. They are more likely to sign on the dotted line once they find the home they are looking for, which could potentially mean a swift sale with fewer contingencies.

Advantages for Buyers

Take advantage of this season to score a bargain

Because more buyers are likely to house hunt during warmer weather, home prices are generally lower in the winter. You can then take advantage of this season and have more buying power since sellers are motivated to sell their home and move before the year ends.

However, don’t assume that you can automatically score a sweet deal. What you can do is use the seller’s motivation to negotiate a bargain. This is particularly in markets where there’s generally less interest and the seller already feels some pressure. They might be more willing to accept an already good offer rather than waste time waiting for a better one. Work closely with your real estate agent to give a good offer and secure a quick settlement.

You can use your end-of-year financial bonus to enter the housing market

The end of the year also means many employees or workers will get their performance reviews, which could mean receiving financial bonuses and large payouts. If you’re a first-time home buyer, you can use this opportunity to enter the housing market and invest that money in purchasing your ideal home, especially if your credit is already in good standing. Buyers can also use the incentives to upgrade their living situations.

Before starting your house-hunting this season, just remember to avoid too much holiday debt while shopping for gifts for your loved ones. Any new debt can change your debt-to-income ratio and affect your mortgage pre-approval. Keep in mind that buying a home can be your biggest investment, so take note of your priorities especially this holiday season.

This year, Hurricane Florence brought tragic damage to the Carolinas and the Eastern Seaboard. And like recent major storms such as Harvey and Irma, Florence has caused massive flooding throughout the region.

According to the Federal Emergency Management Agency (FEMA), no home is completely safe from potential flooding. And without flood insurance, homeowners have to pay out of pocket or take out loans to repair their home and replace its contents. Flood insurance can mean the difference between recovering and being financially devastated. So why risk it when your largest financial investment is at stake? It can take you less than a month to make an offer and close on your dream home, but rebuilding it after flood damage could take months or even years.

Here are five crucial reasons why homeowners should carefully consider getting flood insurance:

1. Your standard homeowner’s insurance policy does not typically cover flood damage.

Many American homeowners are unaware that flooding is one type of natural disaster that isn’t covered by their standard home insurance policies. In fact, at least 43% of homeowners incorrectly believe the damage from heavy rain flooding is covered under their standard insurance, according to the 2016 Consumer Insurance Survey by the Insurance Information Institute.

Most homes in the counties that were hardest hit by Hurricane Florence in September 2018 were underprepared for the aftermath of the storm. A Washington Post analysis revealed only one in 10 homes has flood insurance.

Since your regular home insurance doesn’t typically cover flood damage, you will need a policy offered through the government’s National Flood Insurance Program (NFIP). The average annual premium for a policy through the NFIP was $866, although it is expected to rise about 8% this year. The program’s maximum coverage is $250,000 for your home and $100,000 for its contents.

2. Your home can be miles away from a floodplain or any bodies of water and you can still be a victim of flooding.

It takes just one inch of water to cause $25,000 of damage to your home, as reported by FEMA. You can live miles away from water and your area may be low-risk, but it doesn’t mean there’s no risk involved. Surprisingly, over 20% of flood insurance claims come from properties outside high-risk flood zones.

While homeowners in high-risk areas are likely required by lenders to get flood insurance, it’s also recommended that those who live in low- to medium-risk areas also consider buying a policy.

3. Flood maps can change!

Here’s a sad truth: floods can happen anywhere. Floodplains and floodplain maps change and evolve. When you bought your home, you may have thought, “There’s no need for a flood insurance policy because I don’t live on a floodplain.” But that doesn’t mean your area will always be low risk.

You can check the site FloodSmart.gov to learn more about the flood risks in your area. It’s also a good tool if you want to get more information about the risks, premiums, and agents near you. Your insurance agent can also be your go-to person during your research.

4. Floods are the most common weather emergency.

Anywhere it rains, there’s the possibility of flooding. And according to FEMA, flooding can occur from hurricanes, tropical storms, cyclones, plain old heavy rains, winter storms, spring thaws, overburdened or clogged drainage systems, or occasionally from nearby construction. It doesn’t even have to be caused by a major weather emergency for your property to be affected.

Likewise, flood insurance can pay whether or not there is a Presidential Disaster Declaration.

5. There is a 30-day wait period before the policy goes into effect.

You can’t wait until a hurricane is bearing down on your area for you to get flood insurance. Most policies have a 30-day waiting period between when you buy the coverage and when the coverage takes effect. So you need to purchase a flood insurance policy at least a month in advance to be eligible for reimbursement.

The only exception to this is when the policy you got was required upon closing on a new home purchase. When an extreme storm hits your area within the 30-day period, you’ll have peace of mind that your new home and its contents are insured.

Bottom Line

Flood insurance premiums vary depending on the home’s elevation, the date of construction, and the relative risk of the area. And while the NFIP program has a maximum of $350,000 in coverage for your home and its contents, you may opt to buy excess flood insurance through a private carrier that would cover an amount above the national program’s limits.

It may be expensive, but don’t skimp on a flood policy and protect your largest financial investment. If you’ve been a victim of flood damage and your home is uninsured, you may get a grant from FEMA or a loan from the Small Business Administration. However, the money you’ll get may not be enough to cover the damage. According to this Realtor.com article, those federal grants are not designed to bring homeowners back to a pre-disaster condition. Insurance can help you get to where you were before the disaster occurred.

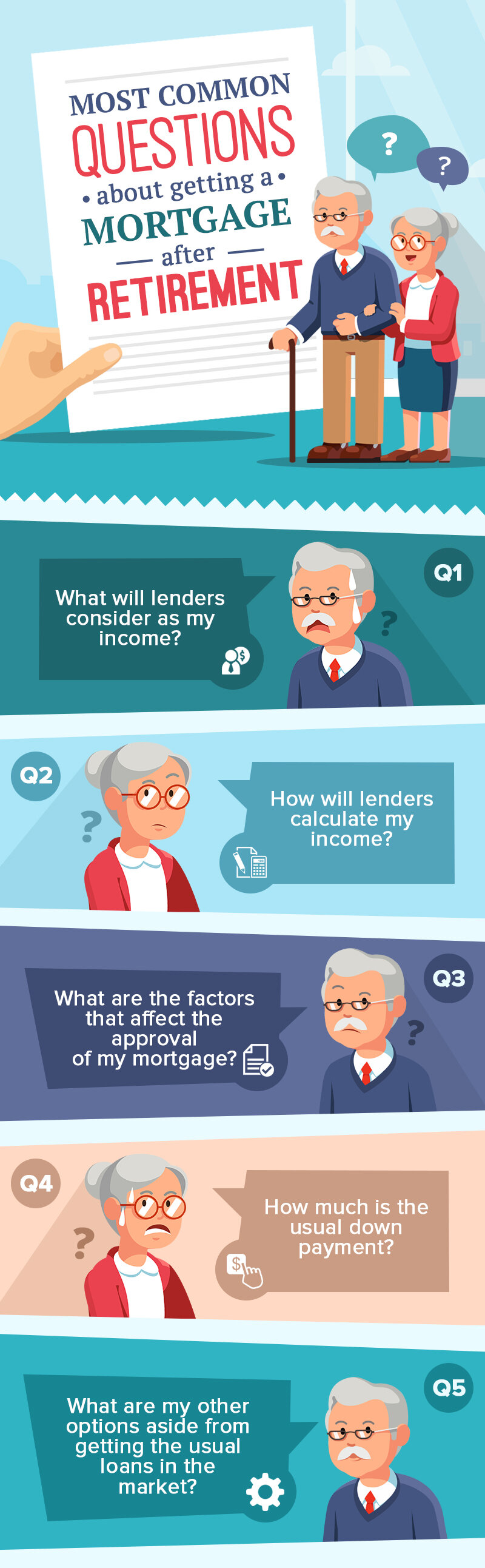

It may seem like a nearly impossible task to get a mortgage after retirement, but there are ways you can do it even if you are not employed. If you’re planning to apply for a mortgage, here are 5 common questions you might ask that we’ve answered for you:

1. What will lenders consider as my income?

Income from a regular or part-time job

A brokerage account or retirement savings

Transfer payments like Social Security and your pension

Invested assets

Household income (income from non-borrowing household members)

2. How will lenders calculate my income?

If you are not employed, there are two methods that lenders will use to calculate your income. Take note that if you receive transfer payments, those will be included in the computation for your income in both of these methods.

Asset depletion method: If you have a lot of invested assets, the lender will calculate their current aggregate value and will subtract the amount for the down payment and closing costs. 70% of what remains will then be divided by 360, which is the number of months’ payment on a 30-year mortgage.

Drawdown from retirement method: If you’re at least 59 ½ years old, you can use documents or receipts that verify your recent withdrawals from retirement accounts.

3. What are the factors that can affect the approval of my mortgage application?

Aside from the above, some of your other financial details will also be subject to the lender’s scrutiny.

Credit score: The typical requirement of lenders for a credit score is usually 780; a score that’s higher than that can increase your chances of getting approved. And if you ever fall short on other factors, such as debt to income ratio, a good credit score just might save your application. Also, if your score is higher than that, you could also get a better interest rate.

Debt to income ratio: Your debt is comprised of car payments, credit card minimum payments and your total projected house payment which includes interest, principal, property taxes and insurance. Other things like alimony and child support are also included in it. The debt to income ratio is expressed as a percentage, and is computed by dividing your total monthly debt by your gross monthly income. The safe percentage among lenders is generally considered to be 43% or lower, but maximum DTI still varies per lender. The ideal is 36%, and with no more than 28% going into paying the mortgage.

House expense ratio: Your housing expense ratio is the sum of your housing payments such as the potential mortgage principal and interest payments, property taxes, mortgage insurance, hazard insurance, and association fees. It’s computed by dividing the sum of those by your pre-tax income. Just like the DTI, it is expressed as a percentage and is ideally not to exceed 36% of your income.

Post-closing liquidity: Your lender would also want to see your available liquid assets after closing, and they usually require that you have assets that could cover at least 6 months’ worth of housing expenses. This is calculated by adding up all of your verified financial assets and then subtracting the closing costs and equity for the loan.

4. How much is the usual down payment?

The amount of down payment you would have to give is dependent on the method used for determining your income.

5. What are my other options aside from getting the usual loans in the market?

VA loans: If you’re a veteran or a military spouse, VA loans offer 0 down payment and low interest rates.

Reverse mortgage: Also known as the Home Equity Conversion Mortgage (HECM) for purchase program, it is a kind of loan that can delay repaying the mortgage (principal or interest) until the house is sold or until the death of the borrower.

Here are some tips for when you’re getting a mortgage after retirement:

1. Getting a mortgage for your primary residence will result in a lower interest rate, while a mortgage on a home that will be used for vacation or investment purposes will have higher interest rates.

2. If you can, make extra mortgage payments. If you can afford to pay more than what the lender calculated, you can arrange to have the monthly payment increased. This can shorten the time you would have to pay for the mortgage and could decrease your monthly payments over time, and decrease the amount of interest you need to pay on the mortgage overall.

3. If you plan to take out a hefty amount of cash for the down payment from an IRA or another tax-deferred retirement plan, take note that you might also be placed in a higher tax bracket.

4. Know about the consequences to inflation hits or a great increase in your property taxes. You also have to consider having a financial contingency plan should there ever be medical emergencies, or a price increase in your health insurance. Take these into account and get an estimate if you can still cover these events on top of your mortgage.

How great does a mortgage payoff sound? After making your final payment, there’s nothing sweeter than seeing in your account that you are already “PAID IN FULL” after a substantial period of 15 or 30 years. Congratulations! Paying off your mortgage is a huge and remarkable milestone—you now own your home free and clear. However, there are still a few things you need to do to ensure that you have a clear ownership of your property. Here are some of those extra steps:

Expect to receive some important documents

When your mortgage is paid in full, your lender should return the mortgage promissory note you signed when you first took out the loan. The canceled promissory note proves you have fulfilled the terms of the loan and that you no longer owe the lender any money. If you don’t receive yours back, the lender should at least send you a payoff notice to show you now have a zero balance on your home.

The lender may also send you the canceled trust deed, which secured your loan with title to your house and which conveys the home to a lender if the borrower defaults. You also need to check your credit report to make sure your mortgage account now shows a zero balance. It may take a few weeks to receive your paperwork, which should include a Satisfaction of Mortgage statement—a document stating that you’ve paid off your home. If you received nothing after a couple of weeks of making your last payment, call your lender to check on your paperwork and make sure it will soon be on its way.

Release of lien

Once you’ve paid off your loan in full, your lender will send a document to the county or city registry office notifying them that your title is now clean. That means the lien the lender attached to the property when you got your mortgage is no longer valid. He/she will prepare a Release of Deed of Trust or Satisfaction of Mortgage that will discharge your property from any claim. When there is no longer a lien on your property, it means all the equity is now yours especially if you decide to sell your home.

Cancel your automatic mortgage payments

If you’re like most homeowners who’ve set up automatic payments through their banks, you now need to contact your bank and tell them to turn off the automatic deduction for your mortgage payments.

Update your payment for property taxes and homeowner’s insurance

For most homeowners, their property taxes and homeowner’s insurance were likely escrowed by their lender and rolled into their monthly mortgage payments. Once you’ve paid off your loan, you’re now in charge of making those payments. For property taxes, contact your local taxing authorities to make sure you’ll receive the bills and avoid a hefty fine if you were late with your payments.

Likewise, for your homeowner’s insurance, contact your insurance company or insurance carrier to have the lender removed from the policy. The lender will no longer have any claim to your house, so they should not have the legal right to any insurance payout in the case of fire and other damage. If your house suffered significant damage and your lender’s name remains in the homeowner’s policy, it can make filing and collecting of an insurance claim more complicated because you’d have to deal with the lender first before you could even get your insurance check.

Now that you’re taking over those payments, you must set aside enough cash to pay for both. Experts highly recommend homeowners to create their own escrow account or open a bank account where they can deposit the funds needed to cover those each month. The good news is that your lender is likely to have kept extra funds above and beyond what you actually owed in taxes (when your payments were held in escrow). You should get that reserved collection a couple of weeks after making your final payment in the form of a check from your lender. You can put that into your account and you can also deposit the same amount as your mortgage each month until you have enough to cover your property taxes and homeowner’s insurance premium.

Keep your documents in a safe place

Well, you’re not exactly at risk of losing your house if you lose your deed. But it can be quite a hassle to replace it. If you do lose it, you can claim a new deed in the county that your house is in by paying a small fee. It’s an important document that signifies your ownership of your home, so better keep it in an actual safe or even in a safety deposit box. It’s also for security reasons just in case things go badly down the road, such as if someone questions your ownership of the property (it isn’t impossible!), or if someone comes claiming you didn’t pay the loan off in full.

Because a mortgage can be your largest financial commitment in life, it’s the last thing you need to pay off before you can consider yourself debt-free. You can finally kiss that debt goodbye for good after making that last payment and allocate the money you were using to pay it down each month towards other financial goals.

You now have some serious cash you can spend whenever you want. But on the wiser side, it’s important to not feel overwhelmed by all these extra cash and miss the opportunities to achieve other concrete goals you are looking forward to, such as a car, a vacation home, and other big purchases. You can also keep part of that money in your bank account or in your retirement fund. If perhaps there are renovations you’ve been dying to do in your home, you can now achieve them and boost its resale value. Or you can make modifications to help you age in place and enjoy the latter years of your life in your beloved home.

Allocating your monthly mortgage payments elsewhere after making your final payment can give you more financial freedom to invest in your home and in yourself. You no longer have to worry that you owe anyone any money. For retirees or those who are nearing their retirement years, it can be one of the best feelings in the world.

Now that the hardest part is over, go treat yourself. You deserve it more than anything. That house is now yours—free and clear of any liens and issues about ownership. It’s an outstanding achievement worthy of a big celebration. In Scotland for an instance, homeowners paint their front door red to signify that they have paid off their mortgage. Go on, paint your door red if you like to. It’s worth proclaiming that you’re now mortgage-free after all these years!

If you’re planning to move away from the city and live a more simple life in the country, take note that it does not come without its unique set of challenges. Here are a few tips to help you when you decide to buy a rural home.

1. Specify your needs and wants.

Before you plan to buy a home in a rural area, it’s best for you to check with yourself what your reasons for buying are. What are you going to make out of this property? Are you using it as a vacation home or a primary residence? Are you going to use the land for agricultural purposes? Do you need your lot to be arable? One way to do this is to make a list of what you need and want your living conditions to be. Include your non-negotiable conditions and nice-to-haves. What you put into this list will help you narrow down the rural areas and properties that would suit you, and would also be of useful information to your real estate agent.

2. Familiarize yourself with the area.

Unless you’ve lived in this area before and decided to move back, the ideal action when you’re moving to an unfamiliar location is to rent in the area first. However, time and other resources can sometimes make that impossible—leaving you with the option to simply do your research on the area. If the agent you hired happens to be from there, you can ask them to give you information but make sure to still do YOUR homework. Here are some items to cover:

Climate and weather

Prevalence of natural disasters

Accessibility to hospitals, fire station, police station, veterinary clinic

Proximity to the town proper or urban center

Food resources native to the area

Local customs of the people

3. Consider the costs of maintaining the property.

The cost of maintaining the property depends largely on the size of the house and the land. The more acres you have, the more you’d have to spend. You’re also going to need bigger tools in place of the ones you have, or you may need ones you may not have while living in the city such as a 4-wheeler truck or a tractor. And remember that the costs are not just limited to the monetary one; you also have to include the cost of your labor in cleaning waste, mowing the lawn, etc. Under certain circumstances, you may also need to consider if you could afford an extra hand in the maintenance. Take all of these into account and deliberate if you could afford and sustain all those expenses for the next 5 years and more.

4. Review utilities.

Utilities in a rural area will differ greatly from those used in suburban areas. An important thing to note is that rural utilities are not tied to commercial systems. Check for each of these utilities and if anything happens to not be within your preference, negotiate with the seller (and the community) how it could be made to suit your needs.

Septic systems – rural areas depend on septic systems for waste disposal. If the house you’re planning to buy is hooked to a septic system, it lowers your taxes because municipalities would only bill those who are connected to a public sewer system. The catch from this is that you may have to replace the system should it break down, and that would be costly. A way to address this is to include a contingency on the septic system requirement of inspections and a septic pump on your contract with the seller.

Power supply – power lines in rural areas tend to be flaky due to weather disturbances

Well water systems – some rural homes could only utilize well water systems instead of a public water source. The advantage to this is that you could cut down on your water bill as water from this is free, and you would only have to pay for electricity that keeps it running. But the downside to this is that it comes from groundwater, and would require tests and routine maintenance in order to make sure that the water is safe for use.

Heating systems – Homes in suburban areas are heated by natural gas, while those in rural areas use either oil or propane. If the house uses oil, the BTU is higher than with gas, and it usually costs less than a gas-fired furnace. But take note that it’s more costly to purchase oil instead of natural gas, and it requires more routine maintenance. Alternatively, if the house uses propane, the average life expectancy is higher than with a gas fired furnace. The drawback to it is minimal compared to the others in that its tank is a sight for eyesore. But that could easily be remedied if you opt to have the tank buried.

5. Clarify what’s included in the sale.

Specify in the contract what feature, building, and structure of the home you think are included in the sale because it could be taken down or away by the seller. At the minimum, and if applicable, the sale should include these:

Existing farm or hunting leases that give (or restrict) other people legal access to be on, farm, graze, hunt on, or camp on your property

Fencing and fence posts

Benches

Bridges

Feeders

Livestock panels

Sheds, which could either be movable or portable

Miscellaneous equipment such as shovels, plows, tractor, etc.

6. Acquaint yourself with local resources.

Ask assistance from local offices regarding issues that you need help on such as property maintenance, ecosystem conservation, etc. Here is a list that could help you with your specific needs:

County USDA Farm Service Agency (FSA) office – After purchasing the property, you have to take the deed to the FSA office to register it and be informed and consequently transfer any Conservation Reserve Program (CRP) or base acre payments to you. They educate rural homeowners through a variety of programs on matters regarding conservation such as erosion control, wildlife habitat, pond construction, and the likes.

Southern States – It’s an established farm co-operative that may help you with guiding you through your concerns regarding agriculture — what the best feeds are, what fertilizers to use, etc. Check if Southern States has a cooperative in your location, or find another supplier if they are not within your vicinity.

Local rural lender – Primarily, they can give you contacts to local lawyers and other service providers such as farming managers and dozer operators. They are also equipped with vital local knowledge that may help you with your concerns.

7. Know your boundary lines.

The step to guarantee how many acres of land you’re buying (and will be taxed on) is to visit the county’s assessor office. They could present you information on the property with a description of its metes and bounds. Check if there is a difference from the original listing and ask the assessor to explain.

8. Check the title insurance.

Inspecting the title insurance lets you know of the issues associated with the property that may not have been disclosed such as the property being recorded as a toxic dump site. There are also other issues that could be attached to it such as unknown or unresolved liens. The county’s recorder can pull up this document for you as it is available to the public.

There are several misconceptions that you might fall trap to when it comes to selling property. If you’re planning to put your house in the market, make sure that you don’t make the following mistakes.

Misconception #1: Organizing multiple open houses will surely bring in more buyers.

Having open houses can be laborious for you as a seller; all that prepping, moving furniture, and showing strangers around can be overwhelming and time-consuming. But that’s no reason to skip it altogether! It has been proven time and again that conducting several open houses could really draw in serious buyers. However, sellers must be wary of some “interested buyers” who go just to open houses as voyeurs: wanting to know how people live, and getting ideas for home decor. The best way to do this is to have a strategy so that your time, energy, and resources don’t go to waste.

Open houses are usually held during weekends, but you can make time for it during the weekdays, as most serious markets are inclined to peak during the week. Also, have your agent make good use of technology to put up your open house dates in apps and websites where homebuyers are set to look for listings.

Misconception #2: Home inspection on your end is a waste of time.

Buyers will most likely subject the house to a home inspection once they’re serious about buying it. But just because buyers are set to do this doesn’t mean you can skip this for yourself. Having your house inspected by a professional before putting it up for listing will help you address issues in the house you might have missed. Also, presenting the home inspection report to prospective buyers will make room for transparency in the transaction — which is always a good thing.

Misconception #3: It is best to decline an offer given right after putting your house on the market.

Sellers normally get overwhelmed after getting a first offer on their home, which then leads to the decision to decline and wait for better offers to come in. However, this is not always the optimal choice in real estate selling, especially in slow markets where it could take weeks or even months to get another offer. If the first offer you get is reasonable and is not below your listing price, then it would be wise for you to consider it.

Misconception #4: Overpricing the home will drive up its value.

As a seller, you want to safeguard your asking price, so it may seem logical to mark it up to make room for negotiations should the prospective buyer ask for a price reduction. Keep in mind that your goal as a seller is to not keep the house in the market for too long, and having it unreasonably priced may do just that. Buyers could be intimidated and may not look at the house in the first place. Be realistic in how you price your home — consider the home’s location, the surrounding properties, and current market conditions.

Misconception #5: It is good to let the house sit in the market for a long period of time to give way for better offers.

There are several factors that keep a property in the market for too long such as poor location or shoddy housing condition. But one common factor is related to the above number: property is not competitively priced, and the seller may be too unrealistic with the asking price that they’re unwilling to level it with market conditions. Remember that having your home sit in the market too long can depreciate it. The longer you persist in selling an overpriced home, the more you’ll encounter buyers with lowball offers.

Misconception #6: Lavish home improvements will increase the value of your home.

While a home improvement can increase your home’s appeal to buyers, keep in mind that doing it does not assure a complete return on investment as you may only recoup a percentage of your expenses. Keep the home improvements practical and minimal; improving your lighting and mowing your lawn can already make a difference without to spend too much.

The process of selling, buying, and moving into a new home can be very complicated and overwhelming. But on the lighter side, it is also a journey full of fun and exciting discoveries. Part of a homeowner’s discovery and realization is finding their ideal neighborhood, their dream backyard, their perfect kitchen, and a wall full of snakes… Wait, what?!

Yes, you’ve read it right. As bizarre as it sounds, homeowners from around the world have discovered many strange and unexpected things on their properties. Some may have lived in their home for a couple of months before encountering weird things, while others already owned their home for years before finding things that are impossible to anticipate. Here we reveal some of the strangest discoveries that happened in our own backyard. Well, you may consider them to be a fun and interesting part of real estate—just don’t forget the hard-earned lessons you can pick up along the way.

1. Some serious cash

Well, the first word you can think of is: lucky, isn’t it?

Artist Josh Ferrin discovered the treasure stashed away in the attic of his home in Bountiful, Utah. When he brought up the discovery—a total of $45,000 in cash and coins—to his family, there was some disagreement on whether they should keep it or return it to its original owners. To teach his two boys the value of honesty, Ferrin returned the money to the previous homeowners despite the thoughts of car and house payments in his head. He says it was a “teachable moment” for his kids that he would never get back again. How cool and sincere was that?

2. World War II love letters

In this digital day and age, sending and receiving handwritten love letters is a practice that can really make your heart melt.

When Zac and Shannon Carter bought a renovated 1970s house in Pensacola, Florida in 2016, the home inspector informed them he discovered a stack of old letters in the original cabinetry. It wasn’t until the Carters moved in that they realized the letters, postmarked from 1948 to 1949, contained a blossoming love story between a World War II veteran and his sweetheart.

They couldn’t help but read the vintage letters and understood that the letters belonged to the original homeowner, veteran William Middleton. Middleton wrote them while he was in school in Georgia after serving in WWII and sent them to a woman named Doreen in Canada. The Carters later learned that the two eventually got married and had children, so they passed on the letters to them to let them read their parents’ wonderful blossoming story.

3. An old cemetery

While the first two discoveries were pleasant surprises, not all homeowners were fortunate enough to encounter such things. This one is quite a good setting for any ghost or haunted story.

Of all the things homeowner Helen Weisensel can find in her century-old home in Jefferson County in Wisconsin, nothing can be as disturbing as unearthing a child’s skull in the basement while they were doing much-needed repairs on its foundation.

They soon found out that her home was built atop an old, long-forgotten cemetery. Archaeologists and local historians even estimated it to be among the earliest burial ground in the county, and more human remains were uncovered.

Subsequently, Weisensel’s nightmare started. She was flooded with pertinent inquiries from her neighbors asking her if she’d experienced weird things happening in her home. And since her remodeling project involved her trying to fix her house and do some serious foundation work, it all became impossible the moment her home was discovered to be an official historic burial ground.

4. Mammoth bones

Unearthing something of a prehistoric significance is already a delight of its own. Well, more so if you made the discovery in your own backyard. When Iowa man John and his two sons went blackberry-picking near a creek on their property in Oskaloosa in 2010, one of his sons noticed what he believed to be a ball in the creek.

That piqued John’s curiosity and interest in archaeology when he realized that the “ball” was no toy—it was actually a 4-foot-long femur of a mammoth dating back as far as 100,000 years ago. That started a historic archaeological event as John’s backyard has become an excavation site, with the University of Iowa’s Museum of Natural History leading the search.

Besides the mammoth’s femur, they had found its feet bones and thoracic ribs. Experts say while it is not unusual to find mammoth fossils in Iowa, it’s a rare find to discover so many bones belonging to the same animal in the same place.

5. A wall full of snakes

Here we have Ben and Amber Sessions, who found what seemed to be their picture-perfect five-bedroom rural home in Rexburg, Idaho. It seemed like a real deal since it was listed for just over $100,000.

Until they found a snake in their yard, which is no big deal since they help keep mice away. But soon after moving, they found dozens more every day. Ben even found over 40 snakes in his yard in a single day. Soon, they also spent sleepless nights listening to what seemed like slithering noises on the walls.

When Ben removed a panel of siding it revealed dozens of snakes living in their crawlspace. Their new dream home was in fact what’s known by locals as “The Snake House.” It was sitting atop an enormous snake hibernaculum, a kind of den where the snakes gather in large numbers to hibernate in winter. What’s more troubling is that they also found out that their tap water (which has a curious taste and smell) was infested with snake musk and feces, a good way for anyone to catch salmonella and other diseases. The Sessions also referred to their home as the “Satan’s Lair.”

The home also had a distraught history of owners leaving in haste after finding out the snaky problem. It turned out that the only way to neutralize the issue of a snake den beneath the home was to raise the entire house off its current foundation and lay down a new concrete foundation beneath it. But that job would cost a massive amount, even more than $100,000 at that time. So in 2009, the Sessionses also ended up abandoning their home and had to file for bankruptcy.

According to real estate experts, the Sessions’ story is a valuable lesson for all home buyers to give importance to due diligence when searching for your dream home.

6. A hidden room full of toxic black mold

Back in 2005, young couple Jason and Kerri Brown with their 2-year-old daughter found a sweet deal in a form of a five-bedroom, two-bath house that was in foreclosure for $75,000 in the cozy town of Greenville, South Carolina.

As they started renovations on the fixer-upper, they removed bookcases in a bedroom when it revealed a passageway that led to a hidden room—a secret corridor!

Well, it can be an exciting discovery for any new homeowner especially if it looks like a passageway towards a hidden world like Narnia. However, it turned out the secret room has a serious mold problem and that the house is contaminated with toxic black mold. What seemed to be a pleasant surprise turned into a nightmare for the young couple.

Inside the room, the first thing they found was a chilling note from the previous owner saying: “You Found It! Hello. If you’re reading this, then you found the secret room. I owned this house for a short while and it was discovered to have a serious mold problem. One that actually made my children very sick to the point that we had to move out.” It was from George Leventis, who’d lived there for a while. After discovering the problem, since he has little money and was unwilling to take the matter to court, he stopped paying the mortgage and moved out. But not without leaving the note to serve as some warning.

The Browns have taken it very seriously and hired an environmental engineer to do further testing. The house’s toxicity levels turned out to be so high they have to permanently cancel their move-in plans and took the serious matter to court.

7. A live artillery shell

There’s the story about our love letters dating back in WWII. Then there’s this realbomb scare for a family who lived in Goshen, Indiana. Wally and Linda DeForests found a live mortar round in their basement as a kind of a housewarming gift after moving into their home in 2010.

Linda initially discovered the approximately foot-long military-grade weapon sitting in a cubby space while she was hanging things on the wall. She even told her husband she found a “torpedo.”

The DeForests have had help identifying what it was from their consulted family friend and army veteran Joshua Blackenship, who kindly explained that it was either a round for a mortar or a lightweight anti-tank weapon.

The family contacted the Elkhart Police Department’s Explosive Ordnance Disposal Unit to come and take it away. Some police officers discerned the old mortar round may have been from the Korean or Vietnam War. Well, it’s a quite a unique way for the DeForests to be introduced in their new neighborhood and be welcomed in their new home.

8. Faberge figurine

Since we started with finding some hard cash, let’s cap off this story with another amazing find. It’s a common thing for many homeowners to display porcelain figurines in their homes, but do you have any idea how much does one figurine cost? A particular figurine was found stashed in an attic in upstate New York of descendants of a gallery owner who bought it in 1934. The tiny statute was unlike no other because it was one of only 50 in existence and was crafted by renowned Russian jeweler Faberge. It was studded in precious jewels and diamond and was sold at an auction for a whopping $5.2 million! Dated to 1912, the particular figurine depicts a personal bodyguard to royalty and was given by Russian Czar Nicholas II to his wife.

Bottom Line

Let’s incorporate the lesson we mentioned in the Snake House story: remember the importance of due diligence. Home buyers should “do their homework” before buying what they’d like to be their dream home. While it can be a time-consuming process, you can ensure that you’ll get the most out of your biggest investment. Many unwanted surprises can be avoided by asking the right questions, hiring an experienced local real estate agent, and giving importance to a home inspection. Following many of those established pieces of real estate advice can help lead you to your ideal property and avoid ending up in a house full of snakes (Yikes!)

Love: Offers a range of amenities and recreational areas

You can have access to a range of amenities being offered by the HOA, such as swimming pools, gym or workout stations, and tennis court. There are also recreational areas for residents, like walking trails, jogging paths, playing fields, and community center.

Hate: Restrictive rules and covenants

While they differ from community to community, each HOA has its own declaration of “covenants, conditions, and restrictions” or CC&Rs. These are the rules that residents have to follow while living in the community. The goals of these rules are not to meddle but to maintain the attractiveness of the neighborhood and the value of the properties. However, some homeowners may find the covenants to be too restrictive or unreasonable since it prevents them from enjoying the freedom they want to have over their home.

Love: Less work and maintenance

Living in an HOA community could mean less work for you as a homeowner. HOAs handle services such as exterior home repairs, lawn care, snow removal, and pest control. They are also responsible for the upkeep of common areas, buildings, and shared amenities.

Hate: You can’t paint, decorate, or renovate your home in the way you like it

Those CC&Rs mean the modifications you can do to your home is limited. Before you can push through with painting your home in your chosen colors, installing a play area or swing set, decorating for the holidays, or adding a new room, you may need to first seek approval from the HOA. If you don’t like someone telling you what to do with your beloved home, an HOA may not be right for you.

Love: The community’s uniform look helps keep home values

The appearance of homes within an HOA must meet the association’s standards, which helps maintain the neighborhood aesthetic and higher home prices. Those desirable amenities can also help increase your home’s value.

Hate: All those associated and mandatory fees

HOAs charge a monthly, quarterly, or annual fee that primarily goes to the maintenance and handling of the common areas and buildings. The fees vary depending on the neighborhood’s location and the amenities being offered.

Love: Handles disputes between neighbors

Rather than getting into a nasty confrontation with your neighbors about their unkempt lawn, noisy dogs or loud parties, you can ask the HOA to handle the dispute on your behalf. The HOA can send them a notice or a warning for any activity that well violates the rules and regulations.

Hate: The threat of foreclosure after missed payments

While laws vary by state, an HOA can move to foreclose on your property if you fail to pay the monthly dues or have delinquent assessments by placing a lien on your property. So make sure your budget can handle those fees so you won’t fall behind on payments and risk losing your home.

Love: The community newsletters

The regular news, tips, and reminders can keep homeowners updated and equipped with valuable information.

Refinancing a mortgage can provide lots of advantages for homeowners. They can lock in a lower interest rate or shorten the term of their loan that can help them save thousands of dollars in their monthly mortgage payments. However, there are still lots of confusion about the refinancing process that hinder them from reaping its benefits. If you’re one of those who have been contemplating if you’ll jump at the opportunity, we debunk the most common refinancing misconceptions to help you decide whether it is a smart choice for you.

“I’m afraid I won’t qualify.”

While there are specific eligibility requirements, many homeowners do qualify for a refinance. Even those who haven’t built up a lot of equity in their homes or are struggling to get their credit back on track might qualify. The guidelines have now loosened up that homeowners who thought they couldn’t refinance before because of credit or employment issues just need to approach a lender to know the process. Don’t let your ‘low financial self-esteem’ stop you before you even get started. For an instance, government programs such as the Home Affordable Refinancing Program or HARP can help you refinance as long as Fannie Mae or Freddie Mac own your loan; it was originated on or before May 31, 2009, and your current loan-to-value ratio is greater than 80%.

“There’s no reason for me to refinance.”

Believe it or not, there are many reasons for you to refinance. The primary reason for many homeowners is to have a lower mortgage rate, which leads to lower monthly payments. It’s also applicable if you want to shorten the life of your loan and save money in interest paid over the life of the loan. Refinancing is also possible for those who have an adjustable-rate mortgage (ARM) and now want to have a low fixed-rate. Homeowners who are planning to stay in their homes for a while can also refinance to fund home repairs and other major purchases.

“It will take too much time and effort.”

Sometimes just the thought of providing the paperwork can be the most daunting part of any real estate transaction. Refinancing is no exception. Many homeowners may find it a burden to provide the documents needed, including pay stubs, tax returns and proof of income (W-2 forms and/or 1099s), credit report, statement of assets and debts, and even title insurance. But if you will think about it, you can easily access most of these requirements anyway if you’ve safely stored them for verification.

If you really cannot locate your copies of those documents and/or you’ve lost them at some point, you can still find that refinancing is worth the hassle. Streamlined refinancing is being offered for homeowners who have government-backed loans such as the FHA, VA or USDA loans. It’s an option that can save them time and money by expediting the refinance process. If you apply for a streamline refinance to simply reduce your interest rate, there may not be a need for a new appraisal or an income verification.

Just remember that while it might not be the case for most conventional loans, the extra time and paperwork can be worth it when you eventually see your monthly payments come down and finally save more cash.

“I can’t refinance with another lender.”

Refinancing is a great opportunity for you to search and compare lenders and mortgage rates so it’s a great opportunity to get a better deal with a new lender. It’s also important toshop around and compare loan options from different types of lenders, such as from a local bank, an online lender, or a mortgage banker. You can also venture out of your town or county when seeking lenders.

“Shop around for rates, and don’t rely on banks in your area,” said Bryan Marsden, editorial coordinator of FatWallet.com.

“I’m waiting for mortgage rates to drop.”

This is a common misconception that most homeowners have about refinancing. Yes, refinancing when mortgage rates are low can be a very smart decision. And yet, there’s no way to know when rates will go lower so it’s quite a gamble to wait every day for it to drop. Opt to refinance depending on your situation, your goals, and whether it makes sense for you.

“I’ve missed my chance to refinance.”

And speaking of waiting for the “right” time, many homeowners think they might have missed their chance to refinance because of rising interest rates. However, experts are saying otherwise. As long as you’re sure on the costs associated with refinancing and confirm that it will lower your monthly payments, it’ll be an appropriate choice for you regardless.

If you think you are moving soon, a refinance isn’t a smart move because you may not recoup the closing costs you spent to save cash on your mortgage payment. Experts recommend that you look for the break-even point of the loan—your total closing costs divided by monthly savings—where you’ll start saving money in your mortgage payments.

Bottom Line

Refinancing may sound complex and overwhelming, but once you know what you’re getting into, you’ll understand that it’s a great opportunity for you to save some serious cash before it’s too late. Remember to choose the right refinancing product depending on your time frame, goals, and plans.

The biggest mistake that both home buyers and sellers could make is skipping or waiving the home inspection due to various reasons, like during a bidding war. And while a home inspection contingency clause is almost always included in a purchase contract, some buyers agree to waive the vital inspections to win their dream home in a competitive market.

Often, sellers skip it to save time and money, not knowing it may leave them little to no time to address any important concerns before they put their home on the market. However, it’s a common ingredient for regret and unexpected costly repairs that could’ve been avoided.

Here are seven valuable reasons why both buyers and sellers shouldn’t skip the home inspection:

Remember that there’s always more to a home than what meets the eye. It may look beautiful and something that exists in a storybook, but the truth is it’s almost impossible to know all about its details and issues. There are ugly homes with problems that are only “skin-deep,” while there are great-looking homes that have bigger problems like termite infestation and mold. These issues can be missed even after multiple showings. Even new construction homes can have issues unknown to buyers that only a home inspection can uncover.

Even after years of living in your beloved home, a home inspection can reveal unexpected flaws that you didn’t even know existed. When did that hole in the kitchen ceiling become so big?Was my dog responsible for all those scratches on the walls? Hidden problems in the foundation, roof, or wiring you didn’t even notice as the homeowner could lead to larger issues.

A home inspection ensures that there won’t be any unwanted surprises in the form of serious safety issues. Through a thorough investigation, both parties can make safety their number one priority. If serious safety issues were found, the seller can promise to make the necessary repairs to guarantee that the home is safe and habitable.

The results of a home inspection can be a great tool for transparency and future planning, especially in estimating future expenses. Buyers can use the detailed findings to plan for future upgrades, calculate for repairs, and carefully prepare their budget once they become homeowners. Meanwhile, sellers can use it to plan for renovations and deal with them as soon as possible. That way, they can continue with the home sale with fewer contingencies and minimal setbacks.

Having a home inspection performed can give you the power to make negotiations with the seller to offer a lower price for the home. Depending on the information gathered, you can include words in your purchase contract requesting the seller to make the repairs. Or if they are unwilling to do so, you can ask them to estimate the costs and take that amount off the final purchase price.

You can use the home inspection report as a leverage when negotiating for a better selling price. By knowing the true condition of your property, you can deal with any problems on your own terms and fix them beforehand. You won’t have to deal with any of the buyer’s request to lower the price or arrange for repairs, which could cost you a huge amount of money or even the sale itself.

While a home inspection can cost a good sum of money, it’s a significant investment that will save you from any costly repairs down the road. Things like safety hazards, pest problems, or water leakage in the basement can end up costing you a lot more money once you already own the home. And all those issues and defects could have been revealed by a home inspector if you only allowed an inspection to push through.

The home inspection phase can be a huge pitfall for both parties in a real estate transaction. Sometimes a transaction doesn’t move forward because the buyer and seller couldn’t agree on the repairs requested from the inspection. A buyer may not feel entirely comfortable with the findings while the seller may refuse to accept more requests. Having a home inspection ahead of time can help expedite the process for both the buyer and seller.

Worst case scenario: a buyer can get cold feet and will not proceed anymore with the transaction if they’re not satisfied with the negotiations after the inspection.

The inspection eliminates all the possible “doubts” and “what ifs” of both parties. Buyers will feel certain and satisfied with their purchase, eliminating buyer’s remorse and giving them a peace of mind. Sellers can also feel confident once the real estate transaction was completed because they can avoid the threat of any legal action due to improper disclosure. A home inspection is a great way to make both the buyer and seller feel positive that they have reached a fair deal in the transaction.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link