Has your house been sitting on the market a while without selling? If so, you should know that’s pretty unusual, especially right now. That’s because the supply of homes available for sale is still far lower than what we’d see in a normal year. That means buyers have fewer options than they usually would, so your house should be an oasis in an inventory desert.

So, if homebuyers have limited choices and your house still hasn’t sold, there’s a reason why. Let’s break one potential sticking point that may be turning buyers away: your asking price.

Especially with today’s higher mortgage rates already putting a stretch on their budget, buyers are being a bit more sensitive about price. As a recent article from the Wall Street Journal (WSJ) says:

“If you are serious about selling your home now, don’t get greedy with the asking price. This is still a seller’s home market as there simply aren’t enough affordable homes for sale in many parts of the country. But with average 30-year mortgage rates above 6%, buyers are much more price-sensitive than they were a year ago.”

Why Setting the Right Price Matters

While you want to maximize the return on your investment when you sell your house, you also need to be realistic based on current market conditions. The simple truth is your house is only going to sell for what people are willing to pay right now.

This can be a hard thing to accept. Especially since emotions can run high during the selling process, which only complicates matters more. After all, you may have lived in this house for years, so it’s only natural you’re emotionally tied to it – and those heartstrings can make it harder to be objective.

But it’s important to acknowledge that a bigger-than-expected price tag deters buyers and may make them dismiss your house as a possibility before even seeing it. And if no one’s looking at it, how will it sell?

If you want to get your house sold, you’ll need to do something to spark interest in your home again. That’s where a local real estate agent comes in. They’ll help use data to find out if it’s priced too high for your local market. They balance the value of homes in your neighborhood, current market trends and buyer demand, the condition of your house, and more to find the right price for your house, so you can close this chapter and start your next one.

Bottom Line

While it’s true there aren’t that many homes available for sale right now, your home’s asking price still matters. And, if it’s not selling, it may be priced too high.

When you read about the housing market, you’ll probably come across some information about inflation or recent decisions made by the Federal Reserve (the Fed). But how do those two things impact you and your homebuying plans? Here’s what you need to know.

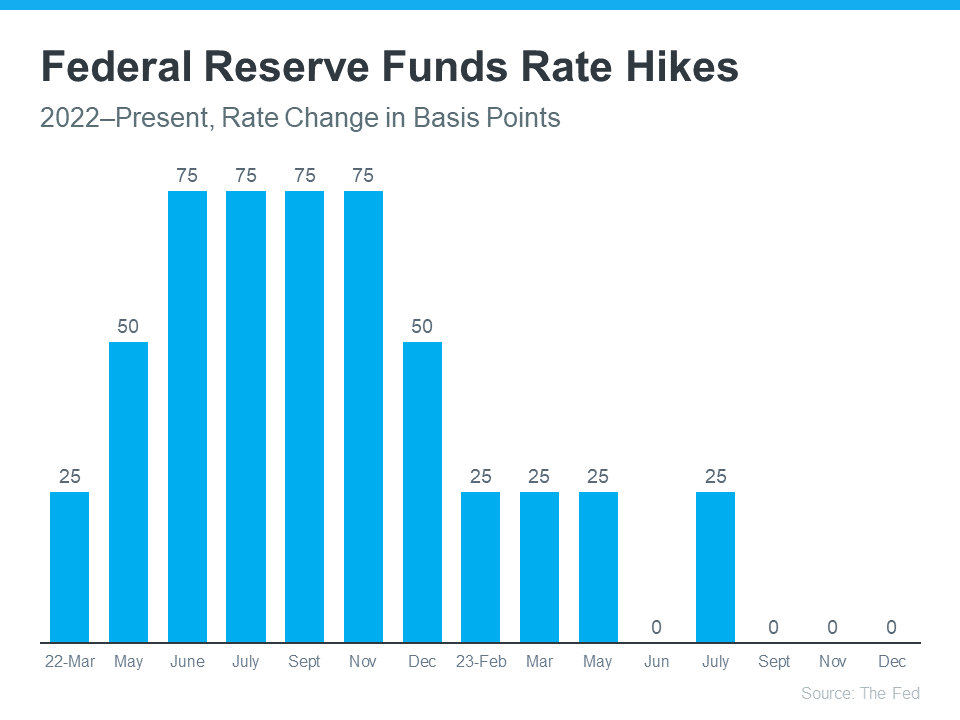

The Federal Funds Rate Hikes Have Stalled

One of the Fed’s primary goals is to lower inflation. In order to do that, they started raising the Federal Funds Rate to slow down the economy. Even though this doesn’t directly dictate what happens with mortgage rates, it does have an impact.

Recently inflation has started to cool, a signal those increases worked and are bringing inflation back down. As a result, the Fed’s hikes have gotten smaller and less frequent. In fact, there haven’t been any increases since July (see graph below):

And not only has the Fed decided not to raise the Federal Funds Rate the last three times the committee met, they’ve signaled there may actually be rate cuts coming in 2024. According to the New York Times (NYT):

“Federal Reserve officials left interest rates unchanged in their final policy decision of 2023 and forecast that they will cut borrowing costs three times in the coming year, a sign that the central bank is shifting toward the next phase in its fight against rapid inflation.”

This indicates the Fed thinks the economy and inflation are improving. Why does that matter to you and your plans to buy a home? It could end up leading to lower mortgage rates and improved affordability.

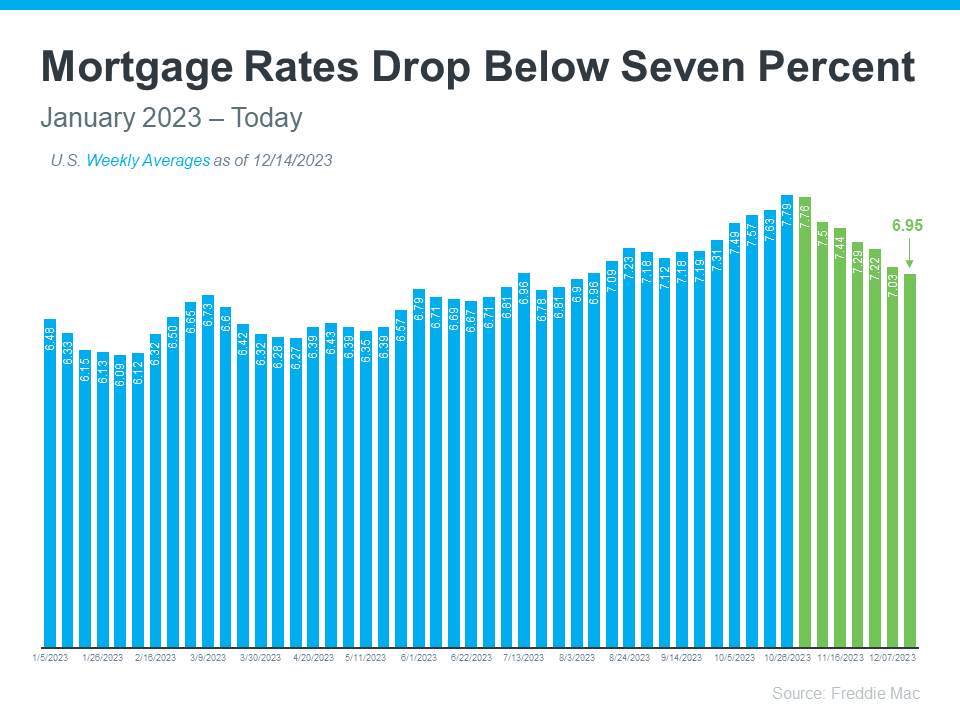

Mortgage Rates Are Coming Down

Mortgage rates are influenced by a wide variety of factors, and inflation and the Fed’s actions (or as has been the case recently, inaction) play a big role. Now that the Fed has paused the increases, it looks more likely mortgage rates will continue their downward trend (see graph below):

Although mortgage rates may remain volatile, their recent trend combined with expert forecasts indicate they could continue to go down in 2024. That would improve affordability for buyers and make it easier for sellers to move since they won’t feel as locked-in to their current, low mortgage rate.

Bottom Line

The Fed’s decisions have an indirect impact on mortgage rates. By not raising the Federal Funds Rate, mortgage rates are likely to continue declining. Rely on a trustworthy real estate expert to give you expert advice about changes in the housing market and how they affect you.

f you’re thinking about selling your house on your own, called “For Sale by Owner” or FSBO, there are some important things to consider. Going this route means taking on a lot of responsibilities by yourself – and that can be a bit of a headache.

A recent report from the National Association of Realtors (NAR) found two of the most difficult tasks for people who sell their house on their own are getting the price right and understanding and performing paperwork.

Here are just a few of the ways an agent helps with those difficult tasks.

Getting the Price Right

Setting the right price for your house is important when you’re trying to sell it. If you’re selling your house on your own, two common issues can happen. For starters, you might ask for too much money (overpricing). Alternatively, you might not ask for enough (underpricing). Either can make it hard to sell your house. According to NerdWallet:

“When selling a home, first impressions matter. Your house’s market debut is your first chance to attract a buyer and it’s important to get the pricing right. If your home is overpriced, you run the risk of buyers not seeing the listing.

. . . But price your house too low and you could end up leaving some serious money on the table. A bargain-basement price could also turn some buyers away, as they may wonder if there are any underlying problems with the house.”

To avoid these problems, it’s a good idea to team up with a real estate agent. Real estate agents know how to figure out the perfect price because they understand the local housing market. They can use their expertise to set a price that matches what buyers are willing to pay, giving your house the best chance to impress from the start.

Understanding and Performing Paperwork

Selling a house involves a bunch of paperwork and legal documentation that has to be just right. There are a lot of rules and regulations to follow, making it a bit tricky for homeowners to manage everything on their own. Without a pro by your side, you could end up facing liability risks and legal complications.

Real estate agents are experts in all the contracts and paperwork needed for selling a house. They know the rules and can guide you through it all, reducing the chance of mistakes that might lead to legal problems or delays.

So, instead of dealing with the growing pile of documents on your own, team up with an agent who can be your advisor, helping you avoid any legal bumps in the road.

Bottom Line

Selling your house is a big deal, and it can be complicated. Having a real estate agent can make a huge difference with setting the right price and managing all the details, so you can sell confidently. Connect with a local real estate agent to make the process smooth and take the stress off your plate.

Even though winter is typically a slow time for real estate, it doesn’t mean it isn’t a good time to purchase a home. Buying a home during this traditional “off” season could work for you depending on the real estate market where you want to move and your personal circumstances.

So if house-hunting has been on your to-do list for a while now, why wait? Forget about the bustling spring and summer months. The winter season can also offer numerous advantages if you’re looking to buy, and here are some of them:

In many housing markets, the off-season typically sees fewer potential buyers in the market, with many of them waiting for the warmer months to purchase a new home. This means you’ll likely face less competition. There’ll be fewer offers leading to fewer bidding wars, giving a higher chance for your offer to get accepted.

Houses that are listed during the off-season often belong to sellers who are eager to close the deal quickly. They may be in a “must sell” situation due to several reasons, such as relocating for a job, financial circumstances, or other life changes that make selling their home the best solution. Thus, they might be more willing to negotiate, whether it’s on price or concessions, such as offering to pay for closing costs.

With fewer real estate transactions taking place during the off-season, real estate professionals such as lenders, agents, inspectors, and appraisers are less busy. For instance, mortgage lenders have fewer loans to process so they can focus on completing your paperwork. This can result in faster response times and a smoother home-buying process, allowing you to move into your new home sooner than expected.

When you buy a home in the spring or summer, you’re seeing homes at their best, in ideal weather conditions. But if it snows in the area during colder months, one of the biggest drawbacks is that you don’t really get a chance to see how the property holds up to low temperatures and harsh weather conditions.

Home shopping during winter will allow you to assess a home’s ability to withstand the cold, moisture, and wind. You won’t only get to see the quality of the insulation and the effectiveness of the heating system. You’ll also be able to check how drafty the windows are, inspect the roof for ice dams, and observe the property for other potential issues that only arise during less favorable weather conditions. By driving around the area during winter, you could also see how well the city clears the roads leading to your neighborhood and your prospective home.

During the busier summer months, many moving companies are already booked weeks in advance. In the off-season, however, the demand for moving services is often lower, resulting in more favorable rates. You might just be able to negotiate a better deal since they aren’t slammed with bookings. It’s also easier to secure their services or rent equipment on shorter notice. Likewise, you’ll have the flexibility to reschedule just in case there’s ice and snow in your area causing havoc on your planned moving day.

Once you close on your new home, you’re eventually going to need new furniture and decor. And there are plenty of opportunities to save when you purchase a home in the off-season. Take advantage of end-of-the-year sales and New Year’s inventory blowouts on major appliances and home improvement materials.

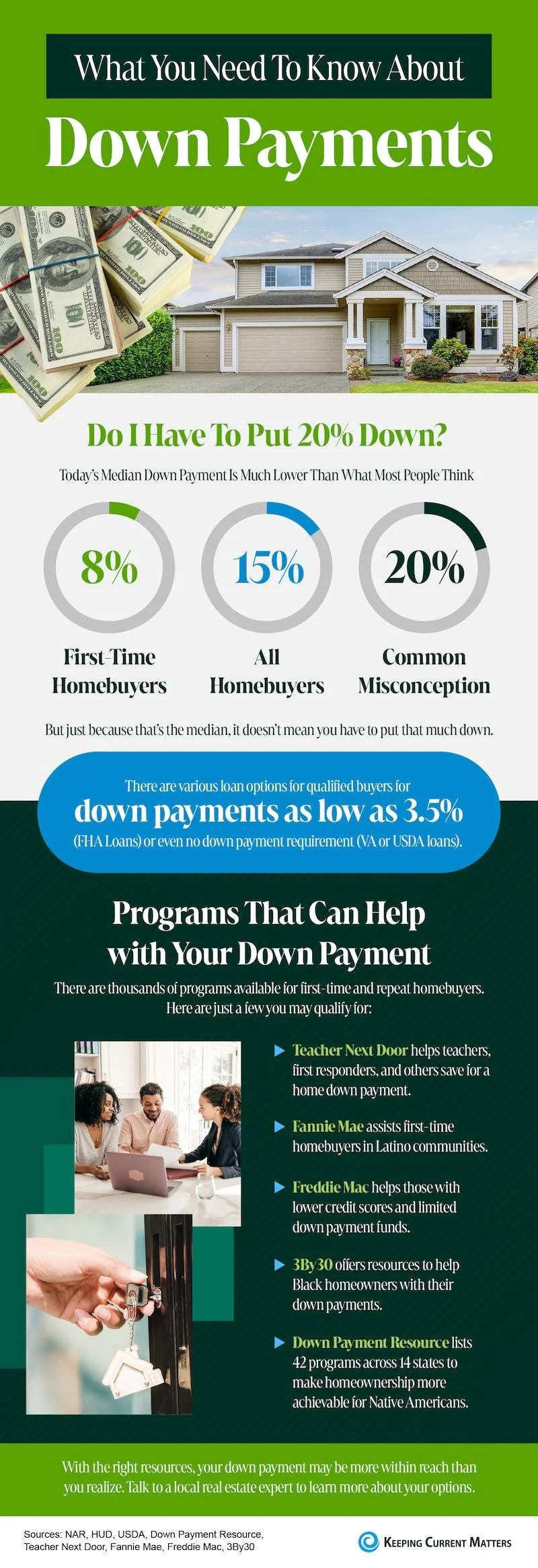

There are various loan options for qualified buyers with down payments as low as 3.5% or even no down payment requirement. There are also thousands of programs available to help homebuyers with their down payments.

With the right resources, your down payment may be more within reach than you realize. Talk to a local real estate expert to learn more about your options.

If you want to have a good neighbor, you have to be a good neighbor first. And learning how to be a good neighbor is a skill that can be equally as impactful on you as it can on your neighborhood.

So whether you just bought a new home or have lived in your place long-term, your goal as a part of a community is to make it a safer and more comfortable place to live in. After all, the quality of a neighborhood is heavily impacted by the people who make it up. Here are six little but valuable practices to help you become the kinder, more caring neighbor you’d want to live next to, not only now that the holiday spirit is in the air, but for the whole year round.

Be mindful of the noise you are making, especially during certain hours of the day, such as late at night or early morning. Avoid blasting loud music, slamming doors, or throwing boisterous parties during those hours. This might be more applicable if you live in a townhouse or a condo, as you likely share walls with neighbors, and noise is more easily heard.

If you’re throwing an evening party, be courteous and let your neighbors know in case it runs late into the night. Do your best to not be disrespectful and disruptive to contribute to a peaceful environment for you and for those who live near you.

We love our furry friends, but not everyone in the neighborhood will feel the same way. Don’t be that neighbor who thinks it’s okay to let their dog bark incessantly day and night. Bring them indoors if they tend to bark through the night and work on improving their habit. If you like taking your pet for walks, always keep them on a leash, no matter their size and breed, in case there are any young children around or people not comfortable with pets. Likewise, don’t forget to pick up after them. Keep your gates locked if they’re out in the backyard to prevent them from escaping. Similarly, don’t let your cat roam the neighborhood and use other’s property as their litter box.

If you’re a new homeowner, understand that everyone in the neighborhood will appreciate you keeping your home’s exterior clean and tidy. Lawn care and yard maintenance are extremely important for most residents, especially those who are concerned about their home’s resale value. And a home that looks like it isn’t being taken care of can unfortunately hurt a surrounding home’s resale potential.

Since you’re now part of a community, one way to contribute to it is by keeping your house in tip-top shape and maintaining a nice curb appeal. Hide eyesores such as trash and other junk, upgrade your mailbox, trim trees and shrubs, etc.—little things that could improve your home’s exterior aesthetics, contribute to your property value and help you stay in good standing with your neighbors.

Another way to be a good neighbor and to take care of your neighborhood is by being helpful. Making small acts of kindness, and helping out whenever you can, benefits both your neighbors and yourself. According to a Nextdoor study, performing small acts of kindness for neighbors reduces the likelihood of feeling lonely. If you see someone struggling with groceries or attempting to do a two-person job alone, might as well offer your assistance. If you’ve living in the neighborhood for a while now, you can help out new neighbors by being a source of information. You can let them know the names of reliable service providers, such as tradesmen, general contractors, or landscapers. Or recommend grocery stores that offer the best deals.

Use the skills and resources available to you when lending some support. Do you have a wonderful garden? Share seeds or seedlings, or even your knowledge on how to grow a particular plant. Remember: every small gesture counts and can go a long way toward establishing yourself as a friendly neighbor.

Getting involved in your community is a great way to show you care, and helps you connect with others, especially those who have the same interests as you. Attend HOA meetings, participate in community events and cleanups, comply with the association’s set of rules, turn up at block parties—generally, take an active role in changing the neighborhood for the better.

It’s natural for issues and concerns to arise between neighbors. Maybe you have a neighbor whose dog barks all night long. Or your next-door neighbor’s tree is causing damage to your property. Or there’s someone who’s clearly not following HOA rules. Whatever the concern, the last thing you shouldn’t do is to complain via text or email, slip them an anonymous note under their door, or badmouth them to other neighbors. It’s best to set a meeting with them to discuss the matters at hand, calmly and constructively. Remain respectful and try to work a solution out that benefits all parties. Most likely, they will appreciate you approaching them directly rather than passive-aggressively throwing them under the bus.

Thanksgiving is easily anyone’s favorite holiday of the year. With each bite of the glorious roast turkey, spoonfuls of delicious mashed potatoes, gravy, and cranberry sauce, and even a slice of pumpkin pie, we are transported closer to Christmas and the spirit of giving.

But with a great feast comes a huge cleanup, which many are not looking forward to. You may be all set and ready for the Thanksgiving dinner, especially if you’re hosting for the first time in your new home, but have you thought about the subsequent cleaning load?

Here are five easy and quick tips to make the Thanksgiving cleanup process easier and ensure the day’s more enjoyable for you and your loved ones.

Need to dig deeper into the home you’re looking to buy? Asking the right questions — and not just the kind that randomly pops into your head — can help you get as much information as you need to put together a competitive offer. Likewise, you will be able to save time, money, and potential headaches if you hit all the necessary topics head-on. It’s part of your due diligence as a buyer, especially since this could be one of the biggest financial commitments you’ll ever make.

If you’re feeling stuck not knowing what else to know about the property, we’ve pulled together a list of some things that may not be so obvious to ask but can get you closer to finding a home that’s a good match for your lifestyle and budget.

Utilities can vary depending on where you live and based on the systems and size of the property. Aside from your monthly mortgage payments, getting an estimate of your monthly maintenance and utility bills is just as important to ensure you can afford to comfortably live in the home.

Especially if you’re a first-time home buyer, it’s best to learn how the home is being heated — by gas, electricity, solar power, or combination — and what the average monthly bill for each is. You’ll also want to inquire about water, waste removal, broadband, and any other applicable maintenance and utility costs. By breaking down information like this, you can have a general idea of how much you’ll spend and incorporate it into your monthly budget.

Have they overhauled the kitchen? Added another room? Broken down a wall? Installed a new HVAC? You’ll also want to know what major renovations the owner has done since it will give you a ballpark idea of how much money they have spent, and what they hope to get out based on a project’s average return on investment. You can also check receipts from contractors to get a sense of what they paid for such upgrades.

But the most crucial reason is for you to guarantee that these additions follow local building codes. Any major improvements—structural additions, installing a new roof, any electrical and plumbing work, or installing/replacing the HVAC system—need to be done by a licensed contractor and be completed to code. Any sketchy renovations and/or mediocre construction can end up costing you money and your health. See whether the seller can produce a building permit for repairs and renovations that require one. If they don’t have the permits or if the work was done by a previous owner, you will need to double-check it with the local building department.

Owning a home means keeping up with its maintenance, which includes looking after each of its components. During showings, don’t forget to ask about the age and condition of the home’s major systems, including HVAC, roof, water heater, and major appliances such as washers and dryers, stoves, and others.

Knowing these early in the process will help you factor in the cost of replacement when looking at the asking price. As a future homeowner, it’s a must to know if something needs to be repaired or replaced soon. Because the last thing you’d want is to find yourself in a situation where you need to shell out thousands of dollars to fix something that you thought was in pristine condition just a few months after moving in.

A roof, for instance, is a major component that’s also very costly to repair or replace. It’s critical to consider how much it will cost you on top of your down payment and closing costs if it’s old and needs repairs. If the roof has existing damage, the lender may require that it be repaired to approve your loan. So if the listing description doesn’t list the roof’s age, make sure to find out so you can avoid a costly disappointment later on.

Additionally, you should ask the seller about the warranty information on appliances; requesting the original manufacturer warranties on any appliances or systems if possible. These will serve as documentation and will give you an idea of their remaining lifespan, as well as their potential replacement costs.

When choosing your first home, don’t forget to check out the parking situation on the property. Will your car(s) fit in the garage? If you and your family have multiple cars, will there be room to park anywhere else on the property other than the driveway? Make sure you ask the rules about on-street parking to avoid fines or high insurance costs.

If you decide to throw a party, will guests need parking permits? How many permits are you allowed to get? Some streets may require a permit, which you may need to apply for. It would also be a good idea to visit the house after work hours and see how crowded the parking is on the street, especially if you live in a busy street which can be more difficult to navigate.

Are there rumors that the property is haunted? Had it been the scene of a crime? Is it located next to a cemetery? Did anyone famous ever live there? In many states, owners are legally bound to disclose if a death or major crime has occurred recently on the premises. You might not care if the house has a reputation or has any associated stories or rumors, but it’s still a good idea to ask around.

There are what they call “stigmatized properties,” defined by the National Association of REALTORS® as any “property that has been psychologically impacted by an event which occurred, or was suspected to have occurred, on the property, such event being one that has no physical impact of any kind.” These conditions could give you room to negotiate a lower purchase price since a house that has some negative associations will often be harder to sell.

Thank you, dear veterans, for your valor, strength, service, and dedication to protect us and keep us safe.

Veterans sacrifice a lot to protect the country. And one way to show appreciation to them and their families is to make sure they know about the mortgage loan that’s available to them: the Veterans Affairs loans by the U.S. Department of Veterans Affairs.

Here are the top four advantages of VA loans:

No down payment – This is the biggest advantage of the loan program. Qualified veterans can purchase a home without making a down payment, no matter how much home they’re buying.

Don’t require private mortgage insurance (PMI) – Unlike other loans that require 20 percent PMI, VA loans do not, allowing military borrowers to save on their monthly mortgage payments.

Limits on closing costs and fees – VA loans actually limit the loan-related costs qualified home buyers can be charged, making home ownership more affordable.

A lifetime benefit – There’s no expiration to this program, and veterans who qualify for a VA loan can use it over and over again.

Bottom line

VA loans are one of the most powerful mortgage options available on the market for veterans, service members, and qualified surviving spouses, which is why it’s so essential to learn about this program and its advantages.

Whether you’re a buyer looking for your first home or a seller preparing to list your property for sale, you’ve probably heard the term “concessions” in real estate. But what exactly does that refer to?

Seller concessions, which are also called seller assist or seller contributions, are the costs a seller agrees to pay to help the buyer when closing on the home. It’s essentially a gift that a seller can offer to reduce the amount future homeowners have to pay out of pocket.

While both the buyer and seller have closing costs they’re responsible for, a buyer’s closing costs are usually 3% to 6% of the home’s purchase price. This is aside from the down payment, which means buyers need to have a good amount of money saved up just to get the keys to their dream home.

To sweeten the deal and close quickly, sellers can either pay a flat percentage of the buyer’s closing costs, or buyers can ask them to cover a specific expense, such as the home inspection or home appraisal. Either way, seller concessions are typically negotiated as part of the buyer’s offer on the home purchase. But while they’re relatively common in real estate transactions, they’re far more likely to occur in a buyer’s market. According to the National Association of Realtors’ 2023 Profile of Home Buyers and Sellers, 20 percent of sellers offered incentives to attract buyers.

Seller concessions can be received on all types of home loans, including conventional, FHA, VA, or USDA loans. However, some rules set limits on the maximum amount that a seller can hand over, depending on the loan type. We’ll discuss more about this later on.

For home buyers, your closing costs will vary depending on your situation. In general, however, you should expect to pay 3% to 6% of the home’s value in closing costs, aside from your down payment. This means you need to have a good amount of money saved up just to get the keys to your dream home. Here are some examples of closing costs and fees that a seller might be willing to cover:

Property taxes

Attorney fees

Home appraisal

Mortgage origination fees

Real estate tax service fees

Title insurance

Mortgage discount points

Inspection fees

Homeowners insurance

Homeowners association fees

Purchase of a home warranty for the buyer

Likewise, a seller concession does not always have to be monetary. It can be other things connected to a home that a buyer may put value into, or anything that can sweeten the deal for the buyer. For instance, a buyer may ask for any existing furniture, appliances, or other loose home items, and the seller agrees to leave them even though they’re not initially included in the sale.

Asking for seller concessions is a part of the negotiation process involved in a real estate transaction. But it’s important to know when sellers may be more likely to offer concessions, and it can be in any of these situations:

It’s a buyer’s market

In this circumstance, sellers have less negotiating power. And since fewer buyers looking for homes than there are houses for sale, sellers can better entice a fair offer by giving a concession.

When the house is overpriced

Instead of having to lower the asking price, a seller may be willing to offer concessions.

When the home has been on the market for too long or it’s been a slow season.

A home that has been on the market for more than a few weeks may raise a red flag to potential buyers. To help sell their home, a seller may be willing to make concessions. The same thing if a seller needs to move during a slow season, especially during the winter months when there may be fewer home buyers.

When a seller needs to move quickly

It may be worth it for some sellers to agree to concessions if they feel it will help expedite the sale of their home, especially if they need to relocate as soon as possible or have already bought a new home, hence paying for two mortgages at the same time.

Seller concessions can benefit both the buyer and the seller. But just the same, it does have possible disadvantages on both sides.

For Buyers

Pros

You could save money on closing costs, which may lighten the financial burden of purchasing a home.

Seller concessions can significantly reduce the capital you need upfront, which could allow you to close the deal.

It can be a good alternative to repairs. If the home inspection report reveals something wrong with the home, and the seller refuses to fix it, providing seller concessions can be a good compensation.

Cons

It could weaken your offer, especially if you’re in a competitive market. If the seller might not be willing to pay some of the buyer’s fees, they might reject your offer quickly.

If you include seller concessions into your loans, the loan balance goes up, which means you could end up paying more over the life of the loan.

Since it can be tricky to determine whether it’s worth it to ask for seller concessions on your own, it’s best to hire an experienced real estate agent who understands the local market and can help you get the best deal.

For Sellers

Pros

Concessions can help sell your property faster, especially if you’re in a hurry to close.

It opens up opportunities for a larger pool of potential buyers.

Cons

You are decreasing their net profit gain from selling the property.

Depending on what you’ll provide as a concession, it can be an added cost you need to consider, which can be a financial burden especially if you’re also in the market to purchase a different home and have closing costs of your own.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link