Owning a home can bring you joy and a sense of belonging. It can improve your psychological wellness, make you more connected to your community, and allow you to customize and improve your living space.

Here are some of the benefits of homeownership in more detail:

Improved psychological wellness: Studies have shown that homeowners tend to have better mental health and well-being than renters. This is likely due to the fact that homeowners feel more in control of their lives and have a sense of accomplishment from owning their own home.

Stronger sense of community: Homeowners tend to stay in their homes for longer periods of time, which gives them more time to build relationships with their neighbors. This can lead to a stronger sense of community and belonging.

Ability to customize your living space: When you own your own home, you can make it your own by customizing it to your taste. This can be anything from painting the walls to adding new furniture or appliances.

If you are considering buying a home, I encourage you to do your research and talk to a financial advisor to make sure that it is the right decision for you. However, if you are ready to take the plunge, homeownership can be a rewarding experience that brings you many years of happiness.

For homeowners who fall behind on their mortgage payments, mainly due to a sudden financial crisis, such as unemployment and other income loss, unexpected debts, interest rate hikes, or economic downturn, among others — the two main options available are either a short sale or foreclosure.

In both cases, the owner is forced to part with their hard-won investment, turning their homeownership dream into a nightmare.

Let’s take a closer look at what these things are, their differences, and which is the better option for any homeowner depending on their situation and timeline.

A short sale occurs when the homeowner or property holder owes more on the mortgage balance than the sale price of the property at the point they want to sell. It happens when the home has substantially depreciated in market value since its purchase. For example, if the homeowner sells a house for $200,000, but still has a remaining mortgage loan balance of $250,000, that would be a short sale. The homeowner or seller is technically “short” by $50,000.

No short sale may happen without the blessing of the lender. Once the short sale is approved by the lender and the property is sold, all proceeds from the sale go to the lender. The homeowner gets nothing and ideally will be free of any financial obligations for the home.

However, one thing to watch out for is the so-called “deficiency judgment”, which the lender can file against the homeowner to make up for the loss. While many states outlaw this practice, it’s critical that you read over your paperwork or ask about it to ensure you won’t have any personal liability.

A foreclosure, on the other hand, is a legal process that takes place when a homeowner (or borrower, in this matter) stops making mortgage loan payments for a significant period of time. After three to six months of missed payments, a lender will issue a Notice of Default with the county recorder’s office. The notice is to inform the homeowner that foreclosure proceedings have started, and they could be at risk of getting evicted.

After receiving the notice of default, the borrower enters into what’s known as the “pre-foreclosure period”, which can last anywhere from 30 to 120 days. During this time, you’ll have the opportunity to work with your lender to avoid foreclosure, either through any of the following:

Paying the past due balance in full;

Modifying the mortgage terms and reducing your monthly payments;

Selling the home through short sale or deed in lieu of foreclosure.

If the debt isn’t resolved by the end of the pre-foreclosure period, the lender will step in and foreclose on the home. The homeowner will be evicted and a foreclosure auction will be scheduled to sell the house to a third party. If the property isn’t sold at auction, the lender becomes the owner and it’s then considered a bank-owned or real estate-owned property.

Have you been browsing homes online, dreaming about the day when you can finally have a place you can call your own? But the thing is, you think you’re not quite ready to buy anytime soon, especially if you haven’t saved up as much money for a down payment as you’d like.

Even if you’re still a few years away from buying a home, there’s a key step you can take that can be incredibly valuable: talking to a mortgage lender. Here are three great reasons you should be having a conversation with a lender even before you begin the house-hunting process.

While you can do your research about various types of home loans online, talking to a mortgage professional is still the best way to widen your knowledge. Even if you’re still months or years away from buying a home, a lender can help you understand the complicated jargon surrounding mortgages. They can also help you start thinking about which type of loan is best for your situation. A lender can also educate you on the different home buyer grants and programs you may be eligible for, especially if you’re a first-time buyer.

When applying for a mortgage, lenders may look at your credit report, credit score, income statements, and other documents that are relevant to your financial situation. If your financial picture is less than perfect, meeting with a lender can get you a headstart so you can make the necessary improvements. You may need months or years to repair your credit, pay your debts, or save up for a down payment, so the earlier you start, the better. Improving your credit score can help you lock in a lower interest rate and qualify for loan programs.

Moreover, remember that aside from a down payment, there are several upfront costs you’ll need to prepare for when you’re buying a home. Working with a lender can give you a clearer idea of what else you’ll need to budget for and how much they’ll cost, including lender fees, title and insurance, appraisal fees, and other closing costs.

There’s nothing worse than finding the perfect property, only to find out that it’s outside your price range. So don’t wait until the last minute to talk to a lender to know what you may or may not qualify for. A lender can help you understand exactly how much you can afford, based on current interest rates, your down payment, and other factors. This way, you can avoid wasting time, energy, and money looking at homes that aren’t within your financial reach. This little pre-work can go a long way to help you be aware of your purchasing power and the competition within the local real estate market.

Completing the sale of a home is a significant accomplishment for any homeowner. After what could be months of preparing, staging, home showings, and negotiating, it can feel like a significant weight is finally off your shoulders. It’s finally time to move on and celebrate, right?

However, even after you close on your home sale, there are important steps that sellers still need to take. In this blog, we discuss some of the crucial things sellers should accomplish post-sale — a checklist to help you avoid potential legal or financial issues and ensure a successful transition so you can move on to the next chapter of your life with ease.

1. Organize your paperwork.

Although this isn’t a fun task, keep your paperwork in order. Save every single piece of paperwork relating to the sale of your home because you’ll need the documentation when it comes time to do your taxes. Your post-sale paperwork typically includes home maintenance receipts and warranties, seller disclosures, listing agreements, and purchase offer, among others. And remember that even after your tax return is filed, you will still want to keep these records in case you’re audited.

2. Know the tax laws.

Since tax laws constantly change, you may want to stay on top of your tax laws to avoid losing money. And hire a trustworthy accountant if you haven’t got one yet. You’re definitely going to need their services come tax time.

An example of a tax benefit is if the house is your primary residence and you have lived in it for two out of the last five years, you’re eligible for a $250,000 exemption on capital gains tax if you’re single, or $500,000 for married people.

3. If you aren’t purchasing a new home right away, consider putting your proceeds in a money market fund.

If you sell your house and don’t immediately buy a new one, you’ll need a safe place to put your money. Consider investing your proceeds in a money market mutual fund, which offers safety and gives a reasonable rate of return. It also allows access to your money if you need it, such as when you’re buying your next home. Money market mutual funds are an attractive option for many people who sold their homes.

4. Consider carefully whether you’ll hire your listing agent when buying your next home.

Buying and selling a home requires a different set of skills and approaches, which is why most agents prefer to specialize as either a buyer’s or seller’s agent. Your agent who helped sell your home may have done an excellent job, so you may be tempted to save yourself some stress and just rehire them to help you with buying. But if you’re relocating to an entirely new neighborhood and looking for a different type of property, you may want to find an agent who is knowledgeable in that area.

If you think your listing agent can also be a good buying agent and you’re moving within the community and in a similar type of property, you may interview your trusted listing agent as one of the three agents you’re considering hiring to help buy your next home.

5. Send change-of-address notices.

Changing your address is a critical task once you’re confident that your home sale will close.

To have your address changed, simply go to the U.S. Postal Service (USPS) website. It is recommended that you do this 30 days before you move to ensure timely forwarding of mail after the date of the move. Moreover, don’t forget to also alert the following parties about your change of address:

IRS

Social Security Administration

State Motor Vehicle Office

State Election Offices

Billing companies (credit and charge cards, cell phones, loans, among others)

Places of employment

Magazines or publications subscriptions

Family and friends

6. Cancel and transfer all of your utilities.

You do need to allot some time to cancel or transfer your utilities, but make sure you do this the day after your home has closed. Turning off utilities on the day the buyers do their final walk-through may cause your closing to be delayed and could even mess up the sale. So wait until a date after closing to call all of your utility companies and request that all services be turned off and transferred out of your name so the buyer can take them over.

The euphoria that comes with purchasing and moving into your first home is unlike no other. You will soon be able to personalize your bedroom, cook in your dream kitchen, or create your version of a backyard oasis. But oftentimes, the excitement can get the better of you.

And while you have every reason to be ecstatic as a new homeowner, a whole lot can also go wrong if you don’t take the time to think things through. From failing to improve your home’s security, to unwanted paint colors and mismatched furniture pieces and designs, watch out for these five mistakes that first-time homeowners typically make after moving into their new homes, and simple but practical tips on how to avoid them.

It’s such a joyous moment to finally get your hands on the keys to your new home. But before you consider renovating your dream space, there’s one thing you need to do which many first-time homeowners often neglect: changing the locks.

Since you don’t know who else might have the keys to your property, consider replacing any old or damaged locks with new ones that are more secure. You can also add deadbolts and reinforced strike plates to your doors for added protection. It’s an added expense, yes, but it will provide you peace of mind knowing that there’s less security risk for you and your family. Soon thereafter, you might also want to invest in a security system, which can include features such as video cameras, motion sensors, and alarms that will alert you if there is any suspicious activity in and around the home.

Many new homeowners may be unfamiliar with the various systems in their house, such as the heating and cooling, plumbing, and electrical systems. These systems are crucial to the functioning of your home, and it’s important to know how they work to avoid costly repairs down the line.

For example, understanding your heating and cooling system can help you to save on energy costs and prolong the life of your HVAC system. You should know how to change the air filters and adjust the thermostat settings to ensure that your system is working efficiently. Additionally, understanding your plumbing system can help you to prevent leaks and water damage. Electrical systems can also be complex, and it’s essential to know when to call a professional if you experience any electrical issues. By understanding these systems, you’ll know when to call an expert if something goes wrong so you can confidently enjoy your new home.

There’s nothing more exciting than putting your personal touches on your new space, and one thing you might be considering is adding a fresh coat of paint. After all, it will be so much easier to paint your room when it’s still empty or uncluttered before you move in. However, it’s advisable to hold off on painting for a while for a variety of reasons.

You may want to wait as you may need time to adjust to your new home’s lighting. The lighting in your new home may be different from your previous one, and this can affect how colors appear on your walls. It’s also important to consider how your furniture and decor will look with the new paint color.

It’s also possible that there are cracks, holes, or any water damage that you need to address first. These underlying issues with your walls can affect the quality and longevity of your paint job, so it’s important to tackle them before you paint.

Additionally, painting can be a messy and time-consuming process. If you move in and start painting, you may feel overwhelmed and stressed. Also, remember that you might want to use decent-quality paint to prevent wear and tear issues, so this is another expense that needs careful planning and consideration.

A new house means new stuff, right? It’s completely understandable to want to fill it with furniture and decor that reflects your style and personality. But purchasing new furnishings to create a fresh look in your new home without having some sort of a plan can be a costly mistake.

First, major furniture (bed, couch, dining table and chairs, etc) can be expensive, especially if you’re looking for quality pieces that you can enjoy for years to come. And if your budget is already tight after covering the down payment and closing costs, it can lead to financial stress. Consider keeping your old furnishings for a while as you settle into your new home. After living in it for several months, you can get a better feel for what you want and prioritize those furniture and appliances that you really need without draining your bank account.

Whatever renovation projects you’ve been thinking of doing once you’ve moved, resist the urge. Hold back and live in the house for a while to learn all about its perks and quirks. See how the light is reflected in different rooms at different times of the day, how a room is being used as opposed to its original function, or just get to know your home in general. There’s a good chance that the changes you want to make after several months may not even resemble the ideas you had when you first moved in.

Besides, making rash decisions can be expensive and pretty stressful. So make sure you don’t rip out those kitchen cabinets or rush to the store to buy lush trees and shrubs for your bare yard without doing some research first and creating a solid plan. Taking a measured and thoughtful approach to any renovation project will ensure that each decision you make fits your overall vision for your home. And if you’re planning to DIY, know the limits of your skills, and don’t hesitate to hire a good contractor or professional to get the job done.

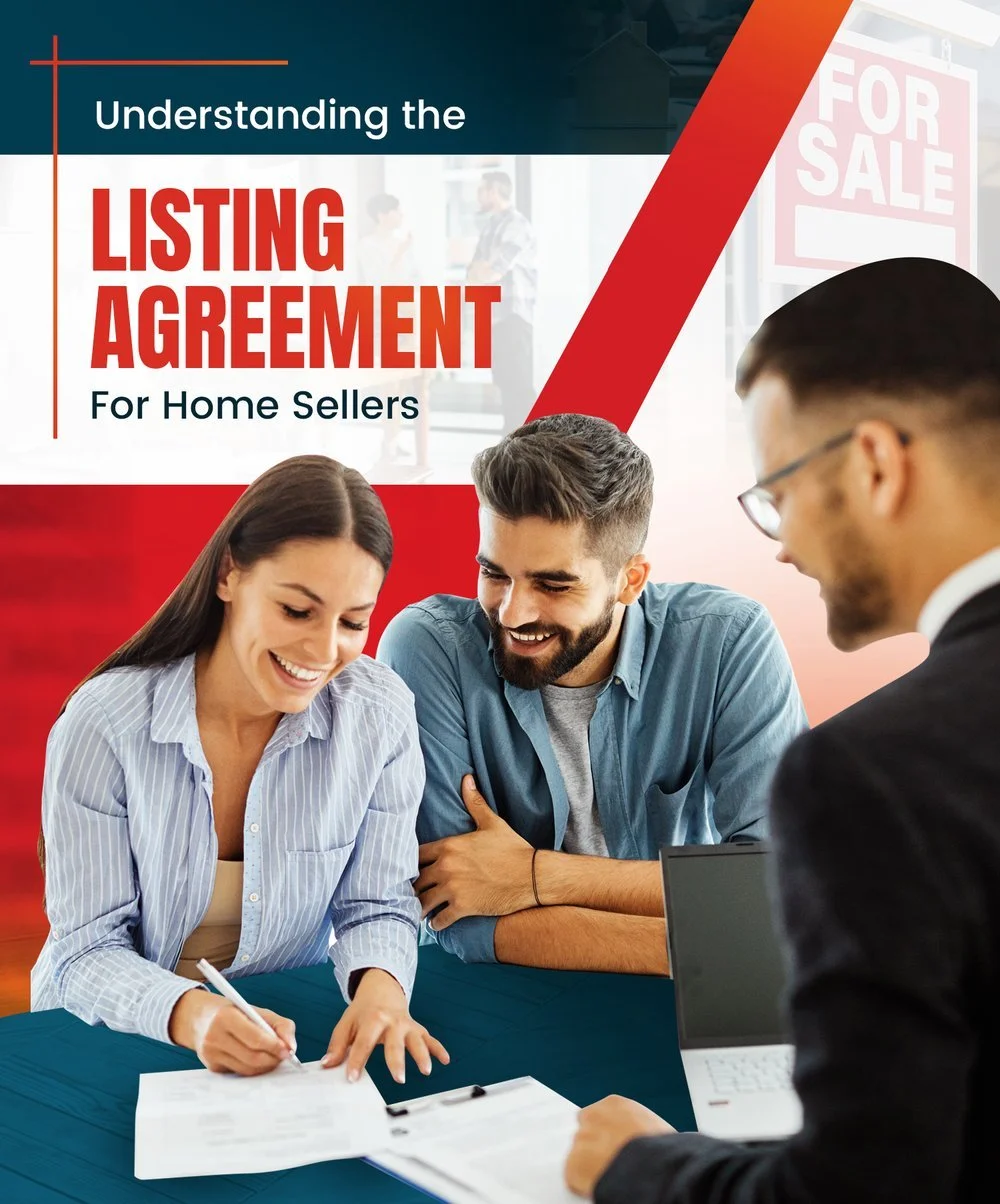

Selling a home can be a daunting task, especially for those who are unfamiliar with the intricacies of a real estate transaction. Even if you’re more than prepared to get your property on the market with a trusted real estate agent, you probably just can’t get down to business without doing this critical step: signing a listing agreement.

Signing any contract can be nerve-wracking and intimidating. But it doesn’t have to be if you understand what the document means. Your agent should also walk you through each part of the service agreement. In this blog post, we’re giving you a headstart to help you understand what a listing agreement entails, and how it plays into selling your property.

A listing agreement is a legally binding contract between a homeowner and the real estate agent or broker who will be listing the property for sale. The agreement outlines the terms and conditions under which the agent or broker will market and sell the home, lays out a framework of duties and expectations between the seller and the agent, and includes several essential details about the upcoming sale.

Only home sellers need to sign a listing agreement. For potential buyers, they will have to sign a buyer’s agency agreement before an agent will represent them. You’ll only sign the listing agreement after you and the agent have agreed on all the details of the home sale. You can think of it as an employment contract, as you are officially hiring the agent for the job of selling your house. No money should be required upfront when you sign, as agents are paid with commission fees at closing.

The listing agreement is meant to protect both parties. It protects the seller by defining the agent’s responsibilities and what to do if he or she doesn’t meet them, preventing you from being tied to an agent that is not fulfilling their end of the service agreement. Meanwhile, it also ensures that the real estate agent is fairly compensated with a guaranteed commission once they execute a successful home sale.

Before we explore the necessary details usually included in a listing agreement, here are the most common types of listing agreements. Your agreement type is often listed at the top of the document itself. The terms can also vary based on the area where you live, so it’s a must to read the agreement closely to understand the specific contract you have with your broker or agent.

Exclusive right-to-sell

This is the most common type of listing agreement. As defined by the National Association of REALTORS®, an exclusive right-to-sell listing agreement is a contractual agreement under which the listing broker acts as the agent or as the legally recognized non-agency representative of the seller, and the seller agrees to pay a commission to the listing broker, regardless of whether the property is sold through the efforts of the listing broker, the seller, or anyone else.

To put it simply, you’ll be working exclusively with one agent to sell your house within a definite period of time. The broker is entitled to their commission regardless of who sells the property, as long as the listing agreement is in effect.

Exclusive agency listing

This type of listing agreement, it’s similar to an exclusive right-to-sell listing where the broker acts as the agent and any agent in the agency may sell the property and collect the commission. But in this case, the seller still reserves the right to sell the home on their own if they choose. And if the property is sold solely through the efforts of the seller, he or she is not obligated to pay a commission to the listing broker.

Open listing

This is a non-exclusive agreement that allows the seller to use multiple real estate agents to sell their home, but the agent who sells the home is the only one who gets a commission. If the homeowner succeeds in selling the home themselves, the agents walk away empty-handed, which is why these kinds of agreements are less common and are generally less favored by agents.

Here are the main components of a listing agreement:

Contact information – includes names, phone numbers, addresses, and other information for the seller and the real estate broker or agent.

Property description – the listing agreement will include a complete and accurate description of the property. The property description also specifies any fixtures that will be left behind after the property is sold, and which items will not be included in the sale and you’ll be taking with you when you move.

List price – You and your agent will discuss the listing price ahead of time, which is based on market data, comparable homes that have sold in the area, and the condition of the home. The price should be written in the agreement to match your earlier discussions.

Agreement duration – a listing agreement usually covers a duration of between three and six months, although it can last for any amount of time you and your agent agree on.

Agent duties – the agent’s responsibilities and detailed plan of action will be specified in this section, together with the activities the listing agent is authorized to conduct on your behalf. This may include holding open houses, listing your home on the MLS, posting a yard sign, etc. Understanding the agent’s responsibilities will give you a clear idea of what they will (and will not) do during the selling process.

Agent commissions – the commissions, fees, and other compensation need to be added to the agreement. Agent commissions are usually between 5 percent and 6 percent of the proceeds of the sale, and are usually split halfway with the buyer’s agent.

Mediation and conflict resolution details – this part of the document states how any potential disputes between the property owner and agent will be resolved. It will specify whether conflicts will be settled using mediation or arbitration, lowering the risk of escalating conflict into a legal dispute.

Protection clause – when the agent shows the house to a potential buyer during the listing agreement period, but that person doesn’t buy the property until after the listing agreement has expired, the protection period clause in the agreement will protect the real estate agent from losing their commission.

While the listing agreement is legally binding, you can make changes to it as needed, which means everything is negotiable. The most common points of negotiation are the listing type, agreement duration, agent duties and commission, and list price, among others. When you make changes to the document, your listing agent will send an addendum highlighting which sections are changed. Both parties will need to sign the addendum for it to be valid. It will then be attached to the original document.

Take the time to review the listing agreement to ensure that all provisions of the contract are correct and include things you and your agent agreed on earlier. Also, make sure that you understand all your agent’s obligations to you, as well as your duties and responsibilities as a seller.

The decision to sell your home is one of the most significant decisions you have to make — both financially and emotionally. The worst-case scenario is that the relationship between you and your agent didn’t work out. Before signing a listing agreement, make sure you are clear on your rights to get out of it if you need to.

You can terminate the listing agreement if you decide that you no longer want to sell your property. Likewise, you can also end the agreement if you do not want to work with your agent or broker anymore and they haven’t found a buyer for your home. Most agents will agree to cancel a listing agreement if the client is unhappy, as long as they don’t have an existing buyer yet.

This is why it’s important to choose a top and trusted real estate agent to help you sell your home. Do your research, interview at least three agents before hiring, and review the fine print before signing a listing agreement with them.

As the weather starts to warm up and the flowers begin to bloom, you might be itching to maximize your outdoor living space. Your backyard is an extension of your home and with the right additions, it can become a functional and relaxing oasis where you and your family can relax and enjoy the beautiful weather.

From practical but stylish options such as shade and outdoor lighting to fun and cozy additions like a grilling station and an outdoor bar cart, we’re here to provide you with plenty of inspiration to help you create the backyard of your dreams.

1. Exterior lighting

Outdoor lighting not only enhances the aesthetics of your space but also improves its functionality. It’s an excellent addition if you aim to create a warm and inviting atmosphere so you can enjoy your backyard even after the sun goes down. It can also highlight certain features, such as a tree or plant, a garden or water structure, or any other architectural elements.

Various types of exterior lighting options include string lights, lanterns, and even pathway or ground lights. Lovely and warm string lights are a popular choice as they add a whimsical touch to your backyard while also providing ambient lighting. Meanwhile, pathway lights or solar ground lights can guide you and your guests safely through your yard while also adding a decorative element. Lanterns can also provide a warm, cozy glow and are perfect for creating a relaxing ambiance.

In addition to enhancing the ambiance, outdoor lighting can also improve the safety and security of your backyard. By illuminating dark areas, you can prevent accidents and tripping hazards. A well-lit backyard is also less attractive to burglars and potential intruders.

2. Hammock

If you’re looking for a cozy but affordable seating addition, a hammock is just the perfect idea. It can be a relaxing spot to unwind, relax and recharge, and enjoy the outdoors while having your favorite book or hugging a warm cup of coffee. When purchasing a hammock, make sure you choose a high-quality variety that is durable, weather-resistant, and can support your weight. Then you can choose to hang them between two trees or posts or get a standalone hammock with its own frame.

3. Bird feeders and houses

Welcome the new spring season into your yard by setting out some bird feeders and houses that will attract a variety of bird species to your backyard, which can be magical to watch and listen to. Since there are many different types of bird feeders and houses to choose from, and each type of feeder attracts different types of birds, it’s a good idea to research which would best suit the birds in your area or those you want to attract.

Aside from having a fun and relaxing activity watching the birds as they come and go from your yard, providing food and shelter for these animals can help support the local ecosystem and promote biodiversity in your area.

4. Canopy or shade

Since the weather outdoors won’t always be ideal — too much sun can be uncomfortable while an unexpected downpour can ruin the fun — creating shade in your backyard is essential. You might want to add an outdoor umbrella, a pergola, or a shade sail to refresh your outdoor living space and keep the area cool.

Outdoor umbrellas are a simple and affordable option that can be easily moved to provide shade where needed. On the other hand, pergolas are a more permanent and stylish option that can add a unique touch to your patio. A shade sail is also an excellent option if you want a modern and sleek look while providing ample shade in specific areas.

5. Privacy screen

If the lack of privacy is what’s hindering you from enjoying your backyard oasis, consider installing privacy screens or outdoor drapery panels to add style and a little extra seclusion from the outside world (and even from nosey neighbors).

There are many options when it comes to adding privacy screens to your backyard. If you want to keep it simple, go with a self-standing screen with vertical or horizontal wood slats, which you can also decorate with trailing flowers or herb pots. Creating a private and comfortable space allows you to enjoy your backyard to the fullest, especially this spring and summer.

6. Grilling station

The warmer weather provides the perfect opportunity to spend more time outdoors, with grilling and barbecues on the side. Setting up a dedicated grilling area spices up your patio and allows you to enjoy outdoor cooking and dining with your family and friends.

Whether you choose to have a simple portable grill or a more elaborate grilling station, it entirely depends on your needs, budget, and yard space. Having an outdoor grill can also provide a fun and enjoyable activity for all ages, with kids helping out in food preparation and adults socializing while the food is cooking. With such a functional addition, expect your backyard to be your new favorite cookout spot filled with wonderful aromas and awesome memories.

7. Outdoor bar cart

Elevate your backyard entertaining game even more by adding an outdoor bar cart. It’s a fancy and stylish way to mix up drinks without using up precious table space or going inside so you can fully enjoy the beautiful outdoors.

Moreover, it’s mobile and convenient to be moved around your backyard, patio, or pool area as needed, making it easy to serve your guests drinks and snacks wherever they are. Or take it even further by setting up a DIY cocktail station where your guests can mix and customize their drinks, adding a playful and social aspect to your backyard gathering.

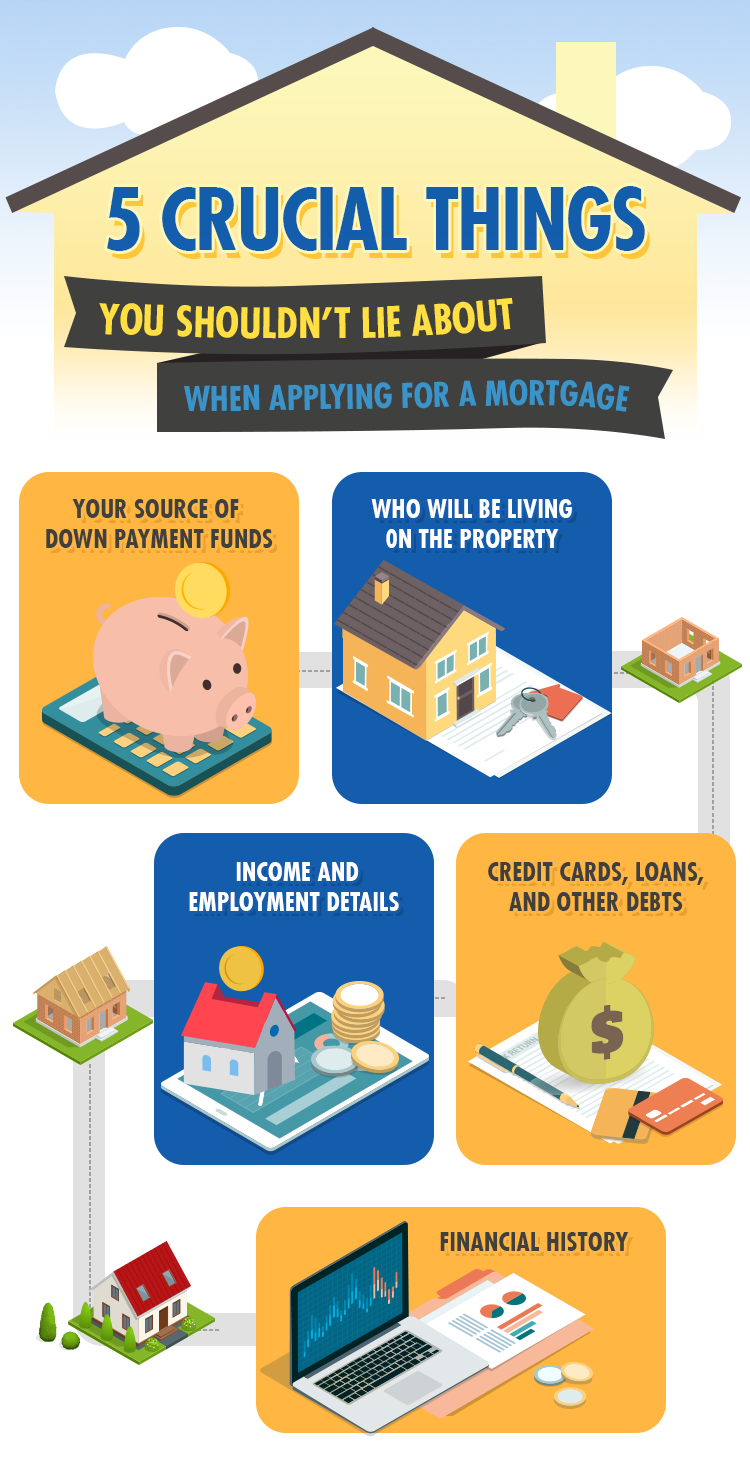

When it comes to applying for a mortgage, remember that there’s no such thing as a little “white lie.” Saying fibs that you think are harmless, as well as exaggerating, playing down, or failing to disclose certain information, can all jeopardize your chances of getting approved for a loan.

Unfortunately, though, about 1 in 131 applications contained some form of fraud, according to the 2022 Mortgage Fraud Report from CoreLogic. Industry experts and risk managers are particularly on the lookout for an increase in income fraud risk.

Here we’ve touched on some of the things borrowers might think it’s okay to lie about during their mortgage application, and why it’s not worth risking your chance to finally buy a home.

1. Your source of down payment funds

For many first-time home buyers, especially younger ones, saving for a down payment is one of the most challenging. Most lenders need to see that you have genuine or regular savings towards a deposit.

If you’ve received help from your parents or any family member for your house deposit, whether it was a gift fund or you borrowed it and plan to pay it back, don’t ever think it’s harmless to declare it as part of your genuine savings. You will have to disclose the source of your down payment to avoid the risk of being questioned, or worse, being denied on your loan.

For down payment gift funds that don’t need to be repaid, lenders may ask for a letter signed by that person, saying that the money doesn’t need to be paid back. But if you’re short on cash and the fund is a loan, lenders will want to know about it because it’s part of your other financial obligations, even if it’s a personal agreement between you and your family member or friend.

2. Who will be living on the property

Unfortunately, occupancy misrepresentation, or lying about who will be living in the property, is common in mortgage applications. You may think it’s okay to claim that the property will be your primary residence when you actually plan to rent it out as an investment property. After all, a loan is a loan and you will be responsible to pay for it, so what difference does it make?

The problem with this, though, is that if you have an investment property, you need an investment home loan instead of an owner-occupied home loan, which comes with lower interest rates and fees. Lenders deem investment properties to be higher risk than residential, as people will usually work harder to repay the mortgage if their own home is at risk. Minimum down payments are also significantly bigger on rental properties.

From the lender’s point of view, you’re stealing money from them by making them take on more risk than they agreed to. So spill the beans on who will be living on the property, as it could amount to occupancy fraud which has serious consequences.

3. Income and employment details

Most lenders require proof of at least two years of stable, long-term employment before granting borrowers a mortgage. So don’t be tempted to say you’ve been working at a company for longer than you do or claim to be employed even when you’re not. Likewise, don’t exaggerate your income to make yourself look more financially stable, or switch employers at any point in the buying process.

Lenders will easily find out because, during the application process, they will request various proof of income documents, including a couple of recent paycheck stubs or tax returns. If something doesn’t add up, be prepared to have to explain. You might still be able to go ahead with your application if you’ve simply made a genuine mistake. But if they’ve found out you’ve downright lied, expect your application to be declined.

4. Credit cards, loans, and other debts

Whether it’s a car loan, credit card debt, or student loan, you need to be upfront about all of your current debts. This is because lenders need to know all your financial burdens to properly assess your financial situation. Failing to disclose your debts, no matter how small, could prove to be a problem later and can hurt your chances of getting a mortgage.

5. Financial history

Lenders will want to make sure that you’ve been consistent with your past payments to deem you trustworthy and make sure you can handle another financial obligation. But if you’ve got a history of late payments, whether it’s missed credit card payments or late loan bills, it’s a must to share that information. Late payments will also remain on your credit report, which the lender will pull during the application process. Likewise, you also need to disclose any bankruptcy, even if it was from years ago.

Even if you think those lies may seem harmless, they come with some serious and expensive consequences. So what happens if you’re found out? Here are some scenarios you might face:

The lender could downright deny your application.

If you’re already under contract, your earnest money deposit could be forfeited.

If the truth comes to light after the deal is done, the lender could decide to call the loan payable. This means you have to pay the full amount of the mortgage, or face foreclosure.

The lender could increase your rate as a penalty, leading to higher interest and monthly mortgage payments.

Worst case scenario: you’ll be charged with mortgage fraud, with a penalty that can include a maximum of 30 years prison time and a $1 million fine.

The biggest lesson: Just be honest from the start so you’ll have a better chance of getting approved for a mortgage.

Hiring a qualified and trustworthy contractor is one of the most crucial elements of a successful home remodeling project. But finding one isn’t easy. Sure, you can ask for recommendations from friends and neighbors, even check online for reviews, but once you’ve put together a list of companies, where do you go from there?

Your home is your haven and one of your biggest investments, so you want to ensure the quality and timeliness of the work. To make a sound decision on which company is the best fit for your project, here are some key questions you can use as a guide during the interview process.

1. How long have you been in this business/industry?

You’d want to get a sense of how much experience the company as a whole has with the work that needs to be done. A contracting business that has been in operation in the area for five or 10 years already has a local reputation to uphold and is more likely to have an established network of subcontractors and suppliers, which makes them a safer bet. They typically have a traceable record, and have created systems and controls to ensure their work is on time and of the highest quality.

But you don’t want to immediately shrug off a new company either, if the company owner or job foreman has years of experience working in the industry, either for other companies or as independent contractors. If you’re impressed with their credentials, you can start by hiring them first for a small repair to check their quality of work. Just remember to do your research ahead of time and verify the credentials of any contractor you’re considering hiring for the job.

2. Are you licensed and insured?

Aside from knowing their years of experience in the industry, you’ll want to make sure that your contractor has gone through all of the necessary certifications to handle the job. And having a business license alone isn’t enough, as it only allows them to operate a business, but it doesn’t guarantee that they are licensed.

A reputable contractor should have any required state license, workers’ compensation insurance, and liability insurance for the type of work they do. Moreso, they should have that documentation on hand and be more than willing to let you take a look. Regulations may vary from state to state and even county to county, so this is a good question to ask to learn more about the contractor and your state’s specific requirements. Doing so will give you peace of mind knowing that they are licensed and certified in their field of expertise.

3. Who is the designated point of contact and how would you like me to get in touch?

Whether it’s the company owner, a project manager, or the job foreman, be sure that you identify a designated point of contact, as well as the best way to reach that person. Ask what times he’ll be available to respond to you, and how quickly you should expect a reply. Remember that communication is necessary for a positive and less stressful remodeling experience, so establishing a defined process with the contractor’s team is critical.

4. Will you obtain the necessary permits and set up the required inspections for the job?

While not every home improvement project requires permits or inspections, it’s a must for large jobs, such as major renovations and anything that involves structural changes. A dependable contractor should not only know what kind of permits you need for the job and how to get them, but they should also be willing to arrange them on your behalf. No work should begin until the permit has been obtained to ensure everything is done to code and your homeowner’s insurance can cover your claim if something goes wrong.

5. Who exactly will be doing the work?

Since contracting companies often work on multiple projects at a time, it’s important to know if they have the workforce to complete the job on time. You should be clear on whether the contractor and their employees will be doing the work or if they’ll be using subcontractors to carry out the project. If they’re using services from another company, you need to know which business they’ve partnered with and who is liable for the work being done, and if the workers are also covered by their liability and worker’s compensation insurance.

Also, clarify whether you can expect to see the same people working on your house to handle the job from start to finish. It’s essential that you can be assured about the consistency of the work, and that you can trust the people you will be working with at all stages of the process.

6. What precautions will you take to protect my property?

While this may be a touchy topic, asking in advance is necessary. Your contractor should be willing to take reasonable measures to keep your property and belongings damage-free. Depending on the scope of work, be sure to inquire about what specifically he’ll do. Are the workers going to wear shoe coverings when they enter the home? Will they use tarps to cover furniture items and surfaces in work areas? They should also be able to recommend certain items that need to be moved to other areas of the house to avoid damage. Moreover, a good contractor will make sure that the end-of-day and end-of-project clean-up is always taken care of.

7. What will be the payment terms and schedule?

Another important detail to discuss with your prospective contractor is the payment terms. You should be aware beforehand of exactly how much is due and when. Payments can be organized by due dates or based on completed stages of the project. Be honest and ask what happens if you are late or need more time to make a payment, as well as the available payment methods.

One thing you need to remember is that a reliable contractor should never ask you to completely pay upfront. Cash payments are impossible to track and are often requested only by questionable contractors. Safer options include checks, loan financing, and credit cards.

House-hunting is no easy journey, especially once you find that there’s a limited inventory of previously-owned homes in the housing market.

If you’re a first-time home buyer, you might find that a new construction house is one of your viable options to finally achieve your homeownership dream. According to the National Association of Home Builders, a full one-third of inventory on the market is now new construction homes.

But if your knowledge of these newly-built homes is still clouded with a lot of misconceptions, we might be able to help set the record straight so you can make a wiser choice based on facts, and decide on the home that’s best for you and your family.

The truth: While they technically cost more upfront, if you look beyond the price tag, you can take into account what you can save by not having to replace, upgrade, or bring to code elements of the home anytime soon.

After all, new construction homes will have brand new roofs, plumbing, flooring, heating and air conditioning, energy-efficient appliances, and other major systems. It’s normal for previously owned homes to have undergone wear and tear of these crucial components. With new homes, it will be years before you have to worry about making any repairs, which could cost tens of thousands of dollars. They also typically come with a warranty, which will cover most repairs in the unlikely event there is a problem.

The truth: Financing a new home can often be easier and simpler. Many reputable builders maintain relationships and/or partnerships with lenders, who tend to be more flexible when it comes to a newly-built home since it translates to less risk compared to a previously-owned home.

The lenders they work with are familiar with the company and the quality of their work so they can quickly get buyers into new homes. Similarly, new construction companies usually have their own lending companies that will offer you several incentives when you do business with them instead of an outside lending source. This can make it easier for you to secure financing and help you get a better deal on your mortgage.

The truth: While they do take time to be built—about seven months on average, according to the 2021 U.S. Census Bureau’s Survey of Construction, this does not mean you’ll need to wait that long.

Many home builders often start building long before they have a buyer. Construction on speculative homes, or spec homes, might already be well underway or even completed before you even start a transaction. You can easily find a move-in ready home if you’re looking to invest as soon as possible.

But still, it would be helpful to do some planning in advance. Make sure to ask how far along the home is in the building process, and if it can be completed within a reasonable time frame. It’s also worth keeping in mind that the build time will vary widely depending on the supply chain, the availability of labor and materials, municipality permitting times, and other factors.

The truth: It might be true for a car, which loses a lot of its value the instant it is driven off. It isn’t applicable to a new construction home, though.

In fact, a new home easily appreciates in value because of price increases as the builder sells more homes. You may even find that you’ve built equity even before you moved in, as more and more homes are sold within the area and the entire community is completed.

The truth: No matter what kind of house it is, the building construction principles generally stay the same.

Regardless of their amenities and features, new homes are still going to be built to a requisite standard and are even subject to the latest in building codes, which have become more demanding over time.

The truth: Home inspections, including new construction properties, are a standard and critical component of buying a home.

While a reputable builder will conduct their own inspection, you can also hire a third-party inspector to ensure the property was built according to the local building code. You can even periodically inspect the home throughout the construction process so you and the inspector can have a better understanding of the home’s condition, and help them to see things they probably wouldn’t once the home is completed.

As a matter of fact, any builder who refuses to allow you to perform a home inspection is a major red flag, since a new build doesn’t necessarily mean it’s free of flaws. New construction houses are also inspected by local municipalities throughout the build, and they’re also the ones who provide a final certificate of occupancy before move-in is allowed.

The truth: You may not be required to have a real estate agent when entering a new construction deal, but there’s no way you’d want to miss out on having your own representation, especially if you’re a first-time home buyer.

As with any real estate transaction, you’d want a knowledgeable and trusted real estate professional who will work in your best interest to negotiate for you on the best possible price, contract terms, add-ons, warranties, target completion dates, and other incentives. Having an agent can help you get the most value for your money and ensure that the transaction is completed properly.

Builders will be happy to work with your agent when you include them early in the process, even before you start searching for new construction homes. When it comes to their commissions, the cost is often part of the builder’s marketing budget when they’re determining the sales price of a home. Besides, not choosing to work with an agent won’t make them offer you a better deal.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link