Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

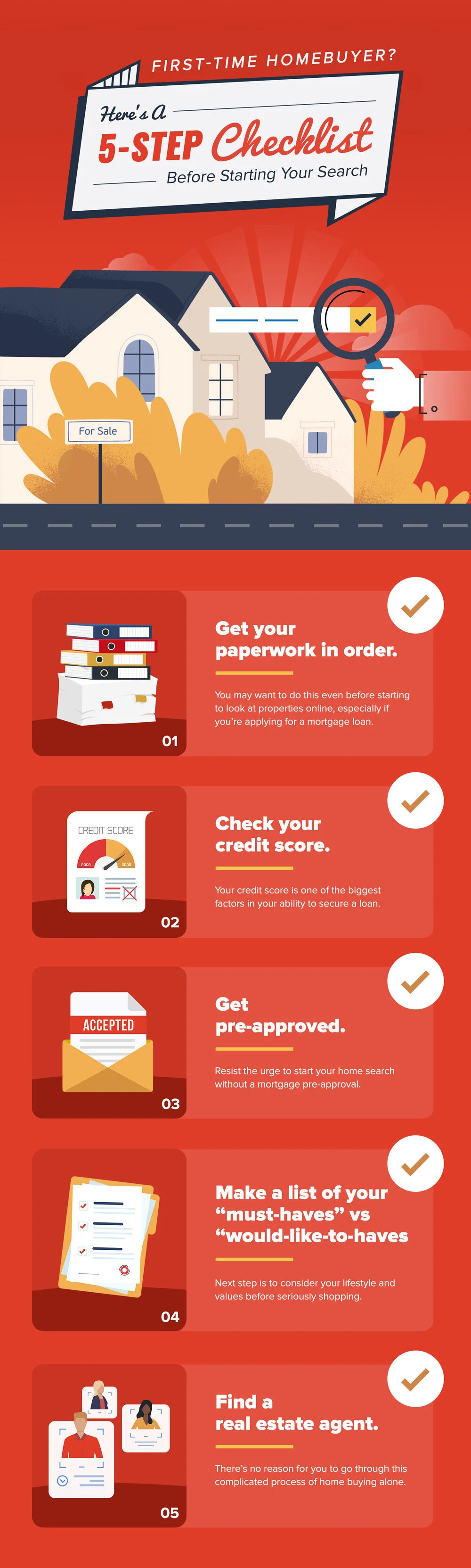

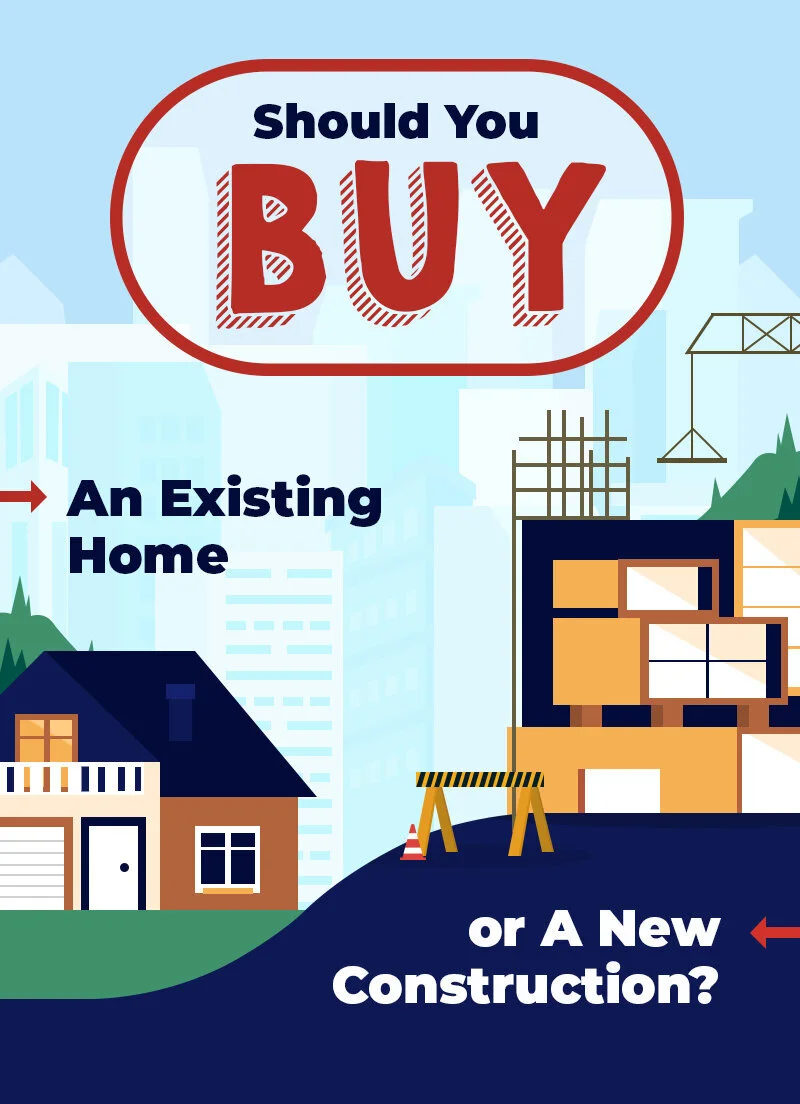

The home buying process involves a lot of decision-making. You will need to make several significant choices, and one of the major ones is whether to look for an existing home or consider buying a new construction.

Many resale homes have a lot of interesting stories to tell, while new construction homes are brand new attractions and may be more energy efficient. Do you love a hand-me-down, or are you the type who prefers anything that is latest?

It’s also worth considering since there’s been a recent decline in the number of homes for sale, while construction of newly built homes are ramping up and builder confidence is soaring, according to the latest Housing Market Index of the National Association of Home Builders.

Whatever it is you choose between the two, remember that for every advantage comes a flip side. This is why it’s important to consider these factors before coming up with a final decision that best suits your needs and situation, which hopefully leads you to your dream home.

While cost always varies by region, there is a substantial gap between the price of a newly constructed home and that of an existing home. The national median for existing single-family homes in the second quarter of 2020 was $291,300, according to the July 2020 Existing Home Sales Statistics by the National Association of Realtors®. Meanwhile, it’ll cost on average $315,282 to build a house, or between $166,237 and $482,652 as per HomeAdvisor. It also depends on the customization and other expensive upgrades you choose to add.

There’s also a greater opportunity for negotiations with the seller when purchasing a resale home, something you generally can’t do if you’re buying from a builder. New construction homes already have a set price for any specific model.

Buyers who are looking to purchase a house with lower maintenance might be better suited for a new construction home. Since you’ll be the first one to live in it, you won’t need to do any significant repairs for a few years or so. Most of the components of the home, including the furnace, water heater, HVAC, kitchen appliances, and others, are brand new and also come with warranties. A brand new home also has more energy-efficient options, especially in appliances, fixtures, and windows, which can help lower your energy costs that could translate to significant savings. If you’re looking to buy a custom home with your preferred style and upgrades, it also eliminates the need for any major renovations later on.

With a resale house, you may need to do some repairs depending on the age and condition of the home. Major issues related to your plumbing, wiring, roof, foundation, air conditioning, or septic system may bring additional costs. You also need to factor in the extra costs of renovations, especially if there are some parts or characteristics of the property that do not suit your taste and needs. You may need to hire a contractor to get the job done or do it by yourself if it’s just a minor renovation. The good thing is that you can make your desired upgrades while you live in the home, whenever you have the time and money to do so.

Timing is something you need to keep in mind, especially if you need to move within a particular time frame because of a change in jobs or other personal reasons. With a resale home, you can move in based on the closing date you agreed to with the seller.

With new construction, you will need to wait for the house to be built, probably around five to six months, unless you’re looking at something that is move-in ready. Of course, a custom home will take several months longer depending on the market and the builder. But with a new construction there won’t be a need to feel rushed or compete with other buyers in the market.

New construction homes are typically built in master-planned communities in the suburbs and exurbs. Land is plentiful but commutes can be longer. Despite this, sales of newly built homes jumped 55% annually in June 2020, according to a monthly survey by John Burns Real Estate Consulting. Factors that contribute to the the increase in new construction sales even during the coronavirus pandemic include a sharp decline in the supply of existing homes for sale, increasing consumer preference for brand-new, high-tech homes with all the amenities for working and schooling, and an accelerating flight to the suburbs and exurbs.

On the other hand, existing homes are commonly located in established neighborhoods, and many are closer to downtown areas where local grocery stores, coffee shops, and restaurants are easily accessible.

Existing homes tend to have more character depending on their architectural style and features. It’s also something to consider especially if you’re looking for the charm that only older homes have.

You also won’t need to grow a lawn or wait for plants and trees to mature since your home will most likely already have landscaping and good curb appeal. With new construction, you might need to create a new landscape, which could mean extra cost.