Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

When it comes to selling your home, it is your duty to disclose things that could be harmful to the future homeowners, such as the presence of asbestos or lead paint in the property, pest infestations, and even mold. However, there are certain facts that sellers should never slip to buyers, especially when it involves personal circumstances.

And while a seller should never be around the house during showings, it isn’t uncommon for the buyer and the buyer’s agent to show up while you are still in the house. And during those short moments when you’re leaving for the door, questions from the buyer such as “Why are you selling?” and “How long has this been on the market?” could be thrown at you. If you’re not mindful of answering these seemingly innocent questions, they could reveal important details that could compromise your negotiating power and cost you the home sale.

Here are some of the things sellers should never, ever talk about with a prospective buyer:

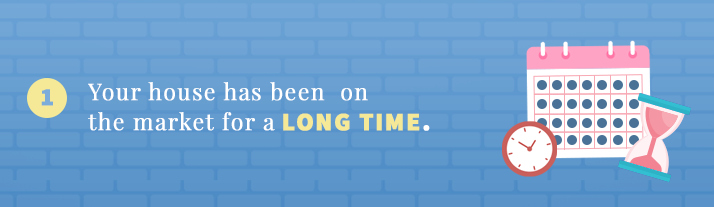

While this information is often listed on the home’s information sheet, you may want to avoid bringing up this topic to potential buyers. Discussing to the buyer how long the home has been on the market can send the wrong message. They may think you’re desperate to sell, so there’s a chance they will give a lowball offer, include too many contingencies, or complicate negotiations. Likewise, buyers may think there’s something wrong with the house that’s why it’s still sitting on the market.

“So, why are you selling your house?”

One of the biggest reasons people sell their homes is out of necessity. You may have lost your job or got an offer to another city; you’re getting a divorce, having financial problems, or had a death in the family. No matter your situation and reason for selling your beloved home, you may want to keep that to yourself. Because while all these situations could evoke sympathy to your potential buyers, it won’t stop them from thinking that you’re desperate to sell.

Remember that the buyer’s goal is to get the best deal possible, and when you hint that you’re going through some difficult times, some buyers may attempt to take advantage of the situation. The last thing you want to show them is desperation. You need to always appear confident so you can fetch top dollar out of your biggest investment.

Each buyer has their own preferences. So avoid saying anything about the neighborhood, or else it could backfire. Informing them that you’d want to move to a peaceful neighborhood could imply there’s a problem with your neighbors or your community in general. Likewise, saying that the area is quiet won’t be helpful either, especially when the buyer wants a thriving nightlife. You don’t know what a home buyer wants in his or her new community so it’s better to avoid this topic.

Don’t disclose that you already found your next ideal home but that your offer is contingent on selling this house. The same rule applies if you’ve already purchased your next home and are already dying to move. While these situations are very common, it may signal to potential buyers that there’s a sense of urgency and you need to sell quickly. And this may prompt them to yield a low ball offer. So instead of sharing that you already found the home of your dreams, tell them that you’re still looking.

Here comes a buyer unconsciously asking, “Would you mind telling me if you’ve had any offers yet?” Your best answers should be, “We’ve had a lot of interest” or “We’re expecting an offer soon.” There’s no need to broadcast how many offers you have or haven’t received, or admit the sad truth that you haven’t entertained a serious buyer since you put your home on the market. You didn’t lie, and these matters should only be between you and your listing agent.

Don’t ever mention anything that you think might be wrong with your home. There’s the temptation, of course, of saying: “We’d always wanted to repair this…” or “We planned to renovate this part of the house but…” Your dreams and “what ifs” for your home and any repairs you planned to address shouldn’t surface now. You may be planting the idea that there’s something wrong with your house. Likewise, if you indicate that the bathroom or bedroom needs renovation, the buyer will think he or she needs to cough up more money, and no matter how good your intentions are, any potential buyer wouldn’t want to entertain any additional costs. They may not even agree with your idea of redoing the bathroom and may love the home as it is.

Who wouldn’t want to sell their house for the best price possible? When it’s time to sell, being realistic to possible price reduction considerations is also paramount. Announcing to your potential buyers that you’re not open to negotiating is a colossal mistake. When you hint that you are inflexible on the home’s price, it may discourage buyers to try to work out on the acceptable price and terms. The worst possible scenario: people may start to avoid the house when words spread that you’re this kind of seller, and your home could sit on the market for a while. Be realistic and open to reasonable offers to increase your chances of putting more money on the table.

Bottom Line

“Loose lips sink ships.“ “Anything you say can and will be used against you.”

These are just some expressions that hold true when it comes to selling a home, and those things, when blurted out, could jeopardize the sale. When you find yourself interacting with a buyer and they ask you questions, just give them short, vague, or neutral responses. Better yet, let your listing agent do all the talking. Part of their job is to handle all communication and negotiations with prospective buyers. If you can’t get away without answering a question, simply tell them that they will have to ask your agent. No more, no less.