Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

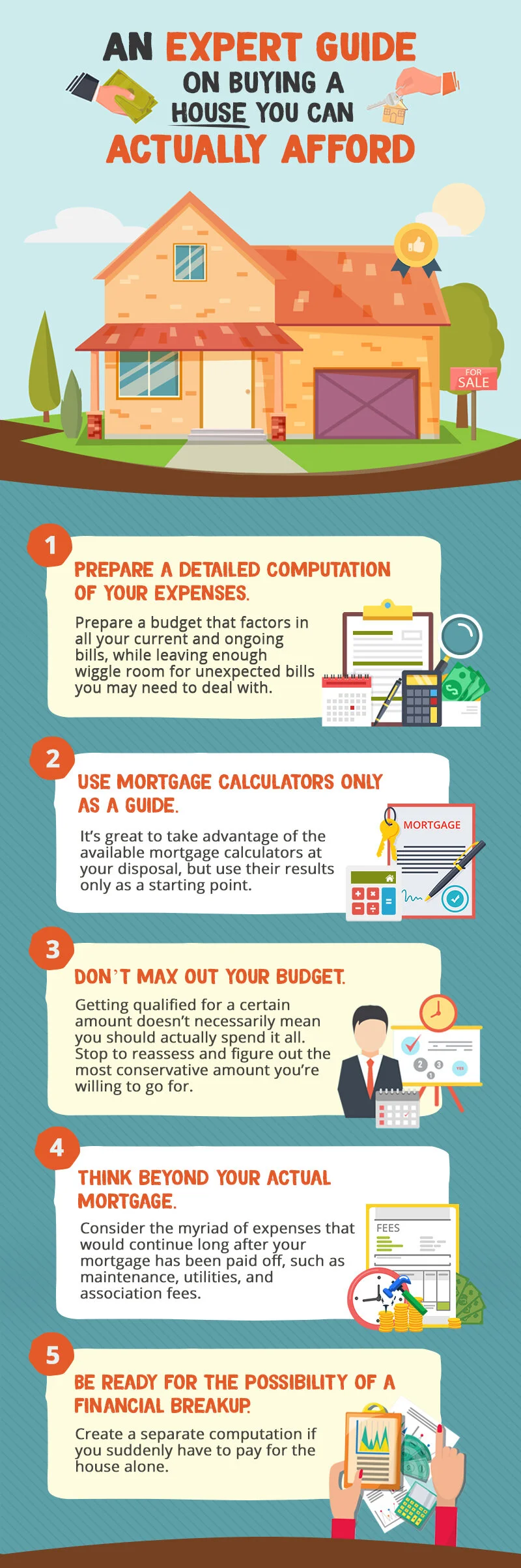

There are several reasons why you are looking at a property outside of your state – you want or need to relocate, you want a vacation home, you’re looking for an investment, or you’re buying for children. As you might know, buying a house isn’t really an easy task, and maybe even more so if it’s not within your local area. The whole process would double your need for time and money resources if you want to be more hands on it. But if that mode can’t fit into your busy schedule and tight budget, here are some tips to help you with buying a house remotely.

-

Hire a good agent.

It’s always important to hire a good agent when you’re buying property because they’re the ones who would communicate in behalf of you to the sellers, would deal with most of the paperwork, have you in the know on some real estate jargon, and optimally, put you up with a good deal on the house of your liking. And if you’re buying outside of your state, they would act as your proxy which means that your agent would have to deal with nearly the entire home-buying process. Do your homework; research and ask for suggestions from trusted friends so that you can make sure that you find an agent that you could communicate well with. You could have a pool of choices and conduct and interview. If you want to know the right questions to ask during an interview, see How To Choose The Right Real Estate Broker.

-

Be clear on what you want, and what you’re buying.

It’s good that you are clear on what you want on your house so that your agent can find properties that are suitable for you. Make a list and give him or her examples of houses with features that fit your needs and liking. But don’t just settle in giving them details about the aesthetics and layout! Also give your agent details about your preferences in the neighborhood, whether you want it close to schools and hospitals or if you want it to be in a tranquil, secluded area. Also, list down things that you want to be sure of will be included in the sale such as fencing and fencing posts, benches, feeders, shelters and livestock pens, existing farm or hunting leases that give other people the right to be on – farm, graze, hunt, or camp on.

-

Map your time.

Consider your schedule. If you could squeeze in a day or two for a trip to the property, that would be good so that you could personally look and check the house. But if your busy life doesn’t permit it, still give it ample time in your schedule to have meetings with your agent and your lawyer so that you can be assured that things are doing well and even if you’re not firsthand dealing with the transaction.

-

Do your research.

Buying a house is a serious task that involves a hefty amount of resources such as time and money, so be sure to be well-informed on what you’re buying. First thing to consider is that you might want to select a property in an area that features healthy housing markets and a strong economy so that your financing doesn’t fall through. Also, if you want to be sure of what you’re buying and will be taxed on, you (or your agent) will need to visit the county assessor’s office. Compare the information on the property from the office with that from what the seller is listing. If you find any discrepancies, talk to the assessor to find out why. Another important matter to consider, especially now that you want to purchase in a rural area is to check their rural resources. Acquaint yourself with the County USDA Farm Service (FSA) office so that you could be familiarized with conservation issues such as erosion control, wildlife habitat, pond construction and other challenges that you may not be ready for as a city dweller. They can tell you about the resources you may need and answer your questions about rural living.

-

Consider renting first before buying.

Moving from the chaos of the city to the peace and quiet of the rural seems like a good and refreshing idea. But sometimes, ideas just look good in your head. If you have the luxury of time and money to test the waters and rent out the house before you buy it, consider doing so. According to Paula Pant from AffordAnything.com, an expert on buy-and-hold real estate investing, it’s worth a try to rent first since housing is an investment that cannot easily be liquidated. She suggests spending at least 6 months in the place. This could brace you and your family for life away from the city. You could also have the chance to familiarize yourself with the area and the house to see if it suits your lifestyle or if it’s worth making a switch in your lifestyle to.

-

Make sure to check the title search and insurance.

If you’re buying a rural property, it’s possible that the land has been listed as a dump-site or a hazardous waste site. Have your agent check the title for the specific property or buy the title insurance so that you can be sure that it’s safe for you to stay in. Another issue that could be addressed by checking into the title is for avoiding liens or encumbrances. This will make sure that the property is really owned by the seller, if there are any tax liens or legal actions against the property.

-

Consider financing matters.

You know that a real estate purchase can be financed using a mortgage. If you want to purchase through this way, have your credit reports ready. The leveraging offered by financing is a huge advantage to you as a buyer, but there are some caveats to consider if you’re buying the house as an investment. According to Bankrate, mortage insurance doesn’t cover investment properties, which means that you have to pay more than 20% of the total purchase price to gain financing.

-

Request a walk-through contingency.

If you haven’t had the time to physically see the property, it’s advisable to negotiate in the contract a walk-through contingency so that if the property does not measure up to expectations in person, you will be safeguarded. Do take note though that sellers are not required to agree to it and may ask for a higher purchase price in order to comply.

-

Know about remote closing.

When you’re about to close the deal, remember that purchase paperwork is full of a lot of lingo that you may not understand as a buyer. Have your agent assist you with those and make some research of your own. Also remember that remote closings hinge on the ability to locate a mobile notary, so you’ll need to ask your lender, agent, or title company for recommendations early on in the process.

-

Have an exit plan.

In case you need to move out for some reason, assess what’s the best option for you to make and consider the time and costs involved. Would it be better to rent the place out or sell it? Have yourself and your trusted agent assess what option could be a better return for your investment.